Prices were up slightly for Scottsdale condominiums in January, but existing-home prices fell 8 percent from a year ago, according to the latest monthly report from Arizona State University Realty Studies.

- Valley's priciest home sales for 2011 | Photos

Foreclosures were down for homes and condos and traditional home sales were up 20 percent.

The Valley's overall median price was $131,660 for homes and $85,000 for condominiums and townhouses.

January 2011

Home sales: 460 (up 12 percent)

Price: $341,195 (down 8.3 percent)

Traditional sales: 325 (up 20 percent)

Price: $370,000 (down 12 percent)

Foreclosures: 135 (down 3.6 percent)

Price: $286,080 (down 0.8 percent)

Condo sales: 270 (no change)

Price: $146,825 (up 1.3 percent)

Traditional sales: 180 (up 2.86 percent)

Price: $146,750 (up 1.2 percent)

Foreclosures: 90 (down 5.3 percent)

Price: $149,770 (up 3.3 percent)

January 2010

Home sales: 410

Price: $372,000

Traditional sales: 270

Price: $420,000

Foreclosures: 140

Price: $288,500

Condo sales: 270

Price: $144,970

Traditional sales: 175

Price: $144,975

Foreclosures: 95

Median: $144,985

by Peter Corbett The Arizona Republic Feb. 22, 2011 09:21 AM

Scottsdale condo prices increase in January

Saturday, March 26, 2011

Housing market's struggles lead to fewer agents

Arizona's struggling housing market, still in recovery mode, has seen a continuing exodus of real-estate professionals.

Not surprisingly, the number of licensed agents and brokers statewide has declined almost 22 percent since 2007, just after the Valley's housing market peaked.

There are roughly 51,000 agents and brokers, according to the latest figures from the Arizona Department of Real Estate.

That is down from more than 65,000 in 2007.

On the flip side, the number of inactive license holders is 19,468, an increase of 48 percent since 2007.

The department does not categorize the license holders by city or county.

The Scottsdale Area Association of Realtors has about 8,000 members and 350 affiliate members.

The state's figures show that there is a 3-to-1 ratio of real-estate agents to brokers, with 38,044 agents and 13,040 brokers.

The number of active real-estate companies in Arizona is 8,748, which is up less than 1 percent from 2007.

The National Association of Realtors reported 1 million members in February, down 5.67 percent from earlier. Its membership in Arizona last month was 39,743, down 3.82 percent from 2010.

Agents fled as market cooled

A lot of people jumped into selling real estate in the mid-2000s, lured by the lucrative commissions on houses that were selling in days, if not hours, well above the listing prices.

But when sales flattened out and agents had to hustle to sell homes, many decided not to pay their $150 to $200 license renewal fees.

Scottsdale agent Rick Amos of Realty Executives said he has noticed there are fewer agents but "what makes up for less competition is more hassles with short sales and more phone calls and explanations to clients."

Those agents that are still at it are more seasoned, he said.

"It helps when you have an experienced person on both sides of the transaction," Amos said.

Exodus of agents worse in past

David MacIntyre, Arizona Best Real Estate owner-broker, said he is surprised there was not an even greater loss of agents.

In previous boom-to-bust cycles nearly half the agents would leave the business, said MacIntyre, who has been in Arizona real estate for 41 years.

His Scottsdale real-estate company still has 115 agents.

And while the luxury market in Scottsdale has been challenged, MacIntyre said he sees it recovering this year.

He sent a dozen of his agents to the Luxury Portfolio Summit in Las Vegas this month to learn about emerging opportunities in high-end real estate.

"The million-dollar buyers are coming back," MacIntyre said, adding that they are paying cash for exceptional values in the Valley.

by Peter Corbett The Arizona Republic Mar. 26, 2011 06:39 AM

Housing market's struggles lead to fewer agents

Not surprisingly, the number of licensed agents and brokers statewide has declined almost 22 percent since 2007, just after the Valley's housing market peaked.

There are roughly 51,000 agents and brokers, according to the latest figures from the Arizona Department of Real Estate.

That is down from more than 65,000 in 2007.

On the flip side, the number of inactive license holders is 19,468, an increase of 48 percent since 2007.

The department does not categorize the license holders by city or county.

The Scottsdale Area Association of Realtors has about 8,000 members and 350 affiliate members.

The state's figures show that there is a 3-to-1 ratio of real-estate agents to brokers, with 38,044 agents and 13,040 brokers.

The number of active real-estate companies in Arizona is 8,748, which is up less than 1 percent from 2007.

The National Association of Realtors reported 1 million members in February, down 5.67 percent from earlier. Its membership in Arizona last month was 39,743, down 3.82 percent from 2010.

Agents fled as market cooled

A lot of people jumped into selling real estate in the mid-2000s, lured by the lucrative commissions on houses that were selling in days, if not hours, well above the listing prices.

But when sales flattened out and agents had to hustle to sell homes, many decided not to pay their $150 to $200 license renewal fees.

Scottsdale agent Rick Amos of Realty Executives said he has noticed there are fewer agents but "what makes up for less competition is more hassles with short sales and more phone calls and explanations to clients."

Those agents that are still at it are more seasoned, he said.

"It helps when you have an experienced person on both sides of the transaction," Amos said.

Exodus of agents worse in past

David MacIntyre, Arizona Best Real Estate owner-broker, said he is surprised there was not an even greater loss of agents.

In previous boom-to-bust cycles nearly half the agents would leave the business, said MacIntyre, who has been in Arizona real estate for 41 years.

His Scottsdale real-estate company still has 115 agents.

And while the luxury market in Scottsdale has been challenged, MacIntyre said he sees it recovering this year.

He sent a dozen of his agents to the Luxury Portfolio Summit in Las Vegas this month to learn about emerging opportunities in high-end real estate.

"The million-dollar buyers are coming back," MacIntyre said, adding that they are paying cash for exceptional values in the Valley.

by Peter Corbett The Arizona Republic Mar. 26, 2011 06:39 AM

Housing market's struggles lead to fewer agents

Bernanke: Overhaul will help small banks

WASHINGTON - Federal Reserve Chairman Ben Bernanke told a group of executives from smaller banks Wednesday that the financial overhaul will level the playing field for them with the industry's giants.

Bernanke said it would be important for the banks to adapt to the changing regulatory environment, in remarks to the annual convention in San Diego of small- and medium-sized banks. Bernanke acknowledged their concerns about the new law. But he said most of the requirements are aimed the country's biggest banks and not them.

Congress passed the regulatory law last year in an effort to prevent a repeat of the 2008 financial crisis. Small-bank executives have complained that it will cost them a lot of money to meet the new rules, even though they were not responsible for causing the financial crisis.

Bernanke said that the hundreds of community banks, those with assets less than $10 billion, would play a vital role in the nation's recovery because they are an important source of loans for small businesses.

"Although we are not yet where we would like to be, the good news is that many community banks have already been doing their part to meet the credit needs of their customers, notably including small business customers," Bernanke said in his speech to the Independent Community Bankers of America.

Bernanke said that it was fortunate that Congress had decided to preserve the Fed's regulatory connection to small banks. In one version of the measure, the Fed would have lost the power to regulate them. But the law maintains the Fed's powers and even broadened it to include thrift holding companies. The thrifts themselves will be regulated by the Office of the Comptroller of the Currency. Congress abolished the Office of Thrift Supervision, which was a weak regulator.

The Fed chairman said the broadened role for the central bank benefits everyone.

In response to an audience question, Bernanke said that the Fed understood that Congress wanted to shield smaller banking institutions from the impact of a new law that requires large banks to trim debit-card fees. At stake is the $16 billion each year that, according to the Fed, stores must pay banks and other credit card issuers when customers use the cards.

The Fed, which must implement a rule to put the new law into effect, understands that banks with assets of less than $10 billion should be protected from losing the fees they now receive, Bernanke said.

Bernanke previously had told lawmakers that the exemption for smaller banks might not work. The concern on the part of the small banks is that merchants might refuse to accept their cards because they carry a higher fee. Bernanke has said that problems in dealing with all the complexities of the new law may mean that the Fed is not able to complete the rule to implement the law by an April 21 deadline.

by Martin Crutsinger Associated Press Mar. 23, 2011 04:44 PM

Bernanke: Overhaul will help small banks

Bernanke said it would be important for the banks to adapt to the changing regulatory environment, in remarks to the annual convention in San Diego of small- and medium-sized banks. Bernanke acknowledged their concerns about the new law. But he said most of the requirements are aimed the country's biggest banks and not them.

Congress passed the regulatory law last year in an effort to prevent a repeat of the 2008 financial crisis. Small-bank executives have complained that it will cost them a lot of money to meet the new rules, even though they were not responsible for causing the financial crisis.

Bernanke said that the hundreds of community banks, those with assets less than $10 billion, would play a vital role in the nation's recovery because they are an important source of loans for small businesses.

"Although we are not yet where we would like to be, the good news is that many community banks have already been doing their part to meet the credit needs of their customers, notably including small business customers," Bernanke said in his speech to the Independent Community Bankers of America.

Bernanke said that it was fortunate that Congress had decided to preserve the Fed's regulatory connection to small banks. In one version of the measure, the Fed would have lost the power to regulate them. But the law maintains the Fed's powers and even broadened it to include thrift holding companies. The thrifts themselves will be regulated by the Office of the Comptroller of the Currency. Congress abolished the Office of Thrift Supervision, which was a weak regulator.

The Fed chairman said the broadened role for the central bank benefits everyone.

In response to an audience question, Bernanke said that the Fed understood that Congress wanted to shield smaller banking institutions from the impact of a new law that requires large banks to trim debit-card fees. At stake is the $16 billion each year that, according to the Fed, stores must pay banks and other credit card issuers when customers use the cards.

The Fed, which must implement a rule to put the new law into effect, understands that banks with assets of less than $10 billion should be protected from losing the fees they now receive, Bernanke said.

Bernanke previously had told lawmakers that the exemption for smaller banks might not work. The concern on the part of the small banks is that merchants might refuse to accept their cards because they carry a higher fee. Bernanke has said that problems in dealing with all the complexities of the new law may mean that the Fed is not able to complete the rule to implement the law by an April 21 deadline.

by Martin Crutsinger Associated Press Mar. 23, 2011 04:44 PM

Bernanke: Overhaul will help small banks

HUD home sale to ban investors

Organizers of a foreclosure-home auction scheduled for Saturday in Phoenix said their event will be unlike any previous home auction in Arizona for one simple reason: No investors are allowed.

BLB Resources, an asset-management firm based in Irvine, Calif., is tasked with disposing of all Arizona homes foreclosed on by the U.S. Department of Housing and Urban Development.

Saturday's auction, scheduled to begin at 1 p.m. at the JW Marriott Desert Ridge Resort & Spa at 5350 E. Marriott Drive in Phoenix, will feature 150 detached homes and condo units in Phoenix, Maricopa, Mesa, Glendale, Buckeye and other Valley communities.

BLB Outreach Manager Ray Warda said it will be the first HUD foreclosure auction his firm has held in Arizona. It also is something of an experiment, Warda said, and it will be unusual because the only eligible bidders are those seeking a home in which to live.

The owner-occupant auction is part of a pilot program BLB is testing in metro Phoenix. If it proves successful for HUD, the seller, there could be more auctions like it in the future. However, Warda said it also could end up being a one-time opportunity.

All the homes were foreclosed on by HUD because the previous owners defaulted on U.S. Federal Housing Administration-backed mortgages.

Requirements to qualify as a bidder include:

- A cashier's check for $1,000, made out to HUD, to be used as earnest money.

- Pre-qualification from a mortgage lender, or proof of adequate financial resources to buy the home outright.

- A valid Social Security number.

- A commitment to living in the property as the buyer's primary residence for at least 12 months.

The auction will be conducted by Phoenix-based auctioneers Hudson & Marshall.

Warda said each home will have an unpublished reserve price that the winning bidder must meet or exceed.

Although the reserve price generally is not disclosed, a number of informational Web sites focused on HUD homes indicate that HUD usually accepts offers at or slightly below a home's current appraised value.

For more on Saturday's auction, visit hudhouseauction.com.

by J. Craig Anderson The Arizona Republic Mar. 23, 2011 06:42 PM

HUD home sale to ban investors

BLB Resources, an asset-management firm based in Irvine, Calif., is tasked with disposing of all Arizona homes foreclosed on by the U.S. Department of Housing and Urban Development.

Saturday's auction, scheduled to begin at 1 p.m. at the JW Marriott Desert Ridge Resort & Spa at 5350 E. Marriott Drive in Phoenix, will feature 150 detached homes and condo units in Phoenix, Maricopa, Mesa, Glendale, Buckeye and other Valley communities.

BLB Outreach Manager Ray Warda said it will be the first HUD foreclosure auction his firm has held in Arizona. It also is something of an experiment, Warda said, and it will be unusual because the only eligible bidders are those seeking a home in which to live.

The owner-occupant auction is part of a pilot program BLB is testing in metro Phoenix. If it proves successful for HUD, the seller, there could be more auctions like it in the future. However, Warda said it also could end up being a one-time opportunity.

All the homes were foreclosed on by HUD because the previous owners defaulted on U.S. Federal Housing Administration-backed mortgages.

Requirements to qualify as a bidder include:

- A cashier's check for $1,000, made out to HUD, to be used as earnest money.

- Pre-qualification from a mortgage lender, or proof of adequate financial resources to buy the home outright.

- A valid Social Security number.

- A commitment to living in the property as the buyer's primary residence for at least 12 months.

The auction will be conducted by Phoenix-based auctioneers Hudson & Marshall.

Warda said each home will have an unpublished reserve price that the winning bidder must meet or exceed.

Although the reserve price generally is not disclosed, a number of informational Web sites focused on HUD homes indicate that HUD usually accepts offers at or slightly below a home's current appraised value.

For more on Saturday's auction, visit hudhouseauction.com.

by J. Craig Anderson The Arizona Republic Mar. 23, 2011 06:42 PM

HUD home sale to ban investors

BofA lawsuit to stay in state court

The Arizona attorney general's lawsuit against Bank of America over alleged mortgage fraud will remain in state court.

The lender had asked the case, filed in late December, be moved to federal court.

State Attorney General Tom Horne, who inherited the lawsuit from former Attorney General Terry Goddard, said state-court cases often move more quickly then those tried in federal court.

"Homeowners who have suffered from practices that may violate the Arizona Consumer Fraud Act need timely relief," he said. "And unnecessary delays can be damaging to them."

The suit alleges BofA deceived borrowers who were trying to obtain loan modifications to keep their homes. The lender is accused of violating the state's consumer-fraud laws by not responding to many homeowners' requests for help, rejecting loan-modification applications without supplying sufficient reason and beginning foreclosure proceedings on homeowners at the same time those borrowers were starting loan modifications.

The lawsuit was filed after a one-year investigation into the loan servicing and foreclosures practices of the Charlotte, N.C.-based lender, Arizona's largest mortgage holder and servicer.

In 2010, nearly 500 consumers filed complaints against BofA. Nevada's attorney general filed a similar lawsuit against the bank on Friday.

BofA has described the filing of the lawsuits as hasty.

by Catherine Reagor The Arizona Republic Mar. 22, 2011 04:42 PM

BofA lawsuit to stay in state court

The lender had asked the case, filed in late December, be moved to federal court.

State Attorney General Tom Horne, who inherited the lawsuit from former Attorney General Terry Goddard, said state-court cases often move more quickly then those tried in federal court.

"Homeowners who have suffered from practices that may violate the Arizona Consumer Fraud Act need timely relief," he said. "And unnecessary delays can be damaging to them."

The suit alleges BofA deceived borrowers who were trying to obtain loan modifications to keep their homes. The lender is accused of violating the state's consumer-fraud laws by not responding to many homeowners' requests for help, rejecting loan-modification applications without supplying sufficient reason and beginning foreclosure proceedings on homeowners at the same time those borrowers were starting loan modifications.

The lawsuit was filed after a one-year investigation into the loan servicing and foreclosures practices of the Charlotte, N.C.-based lender, Arizona's largest mortgage holder and servicer.

In 2010, nearly 500 consumers filed complaints against BofA. Nevada's attorney general filed a similar lawsuit against the bank on Friday.

BofA has described the filing of the lawsuits as hasty.

by Catherine Reagor The Arizona Republic Mar. 22, 2011 04:42 PM

BofA lawsuit to stay in state court

Home market in Valley may rebound soon

Several key housing indicators that predicted last year's double dip in metro Phoenix home prices are now showing the market could be poised to start a slow rebound.

According to "Cromford Report" principal Mike Orr's daily tracking of the region's residential real-estate data, most of the key indicators that turned negative at the end of last year's second quarter are now showing positive signs: Inventory, or supply of homes for sale, has been falling since late November.

Pending listings, a precursor to home sales that tracks buyer interest, has been climbing steadily this year. There were 8,695 pending listings at the beginning of January, compared with almost 13,000 now.

Home sales were up during the first quarter, compared with last year's steady pace.

There are two important market gauges that haven't turned around yet: pending and actual sales prices.

But Orr said the improvement in the other housing indicators could signal prices will climb during the next six to nine months.

Tom Ruff of Information Market, a Phoenix real-estate data firm, shares Orr's opinion.

"The numbers that made us pessimistic last July are the same numbers that are now making me optimistic," he said.

Many homeowners may feel whipsawed by forecasts for a housing recovery during the past few years that didn't happen. But the numbers tracking buyer demand and sales are the ones to watch.

Foreclosure help

Hope Now is hosting another event for Arizona homeowners facing foreclosure. This year's free, daylong session is set for Thursday at the Phoenix Convention Center.

The event is promoted as a chance for struggling homeowners to sit down with housing counselors and potentially someone from their lender to discuss ways they can avoid foreclosure.

At the past event two years ago, some metro Phoenix homeowners received the help they needed but others came prepared with their mortgage and debt paperwork and left disappointed.

Several lenders are signed up to participate, and representatives from Making Home Affordable, Fannie Mae, Freddie Mac, the Arizona Department of Housing, Arizona Foreclosure Prevention Task Force, Department of Labor and Loan Scam Alert will all also be there.

The homeowner workshop begins at 11 a.m. and lasts until 7:30 p.m.

Lender Wells Fargo is participating in this week's homeowner event but is also hosting its own next week, March 30-31.

Wells Fargo's workshop is also at the Phoenix Convention Center and runs from 9 a.m. to 7 p.m. each day.

by Catherine Reagor The Arizona Republic Mar. 22, 2011 07:20 PM

Home market in Valley may rebound soon

According to "Cromford Report" principal Mike Orr's daily tracking of the region's residential real-estate data, most of the key indicators that turned negative at the end of last year's second quarter are now showing positive signs: Inventory, or supply of homes for sale, has been falling since late November.

Pending listings, a precursor to home sales that tracks buyer interest, has been climbing steadily this year. There were 8,695 pending listings at the beginning of January, compared with almost 13,000 now.

Home sales were up during the first quarter, compared with last year's steady pace.

There are two important market gauges that haven't turned around yet: pending and actual sales prices.

But Orr said the improvement in the other housing indicators could signal prices will climb during the next six to nine months.

Tom Ruff of Information Market, a Phoenix real-estate data firm, shares Orr's opinion.

"The numbers that made us pessimistic last July are the same numbers that are now making me optimistic," he said.

Many homeowners may feel whipsawed by forecasts for a housing recovery during the past few years that didn't happen. But the numbers tracking buyer demand and sales are the ones to watch.

Foreclosure help

Hope Now is hosting another event for Arizona homeowners facing foreclosure. This year's free, daylong session is set for Thursday at the Phoenix Convention Center.

The event is promoted as a chance for struggling homeowners to sit down with housing counselors and potentially someone from their lender to discuss ways they can avoid foreclosure.

At the past event two years ago, some metro Phoenix homeowners received the help they needed but others came prepared with their mortgage and debt paperwork and left disappointed.

Several lenders are signed up to participate, and representatives from Making Home Affordable, Fannie Mae, Freddie Mac, the Arizona Department of Housing, Arizona Foreclosure Prevention Task Force, Department of Labor and Loan Scam Alert will all also be there.

The homeowner workshop begins at 11 a.m. and lasts until 7:30 p.m.

Lender Wells Fargo is participating in this week's homeowner event but is also hosting its own next week, March 30-31.

Wells Fargo's workshop is also at the Phoenix Convention Center and runs from 9 a.m. to 7 p.m. each day.

by Catherine Reagor The Arizona Republic Mar. 22, 2011 07:20 PM

Home market in Valley may rebound soon

Tuesday, March 22, 2011

Treasury to Sell MBS Holdings. Minimal Shock Expected

Today, the U.S. Department of the Treasury announced that it will begin the orderly wind down of its remaining portfolio of $142 billion in agency-guaranteed mortgage-backed securities (MBS).

Excerpts from the Presser...

Starting this month,Treasury plans to sell up to $10 billion in agency-guaranteed MBS per month, subject to market conditions. At the end of each month, Treasury will post on its website the total agency-guaranteed MBS sales it has made, broken down by coupon and agency.

“We’re continuing to wind down the emergency programs that were put in place in 2008 and 2009 to help restore market stability, and the sale of these securities is consistent with that effort,” said Mary J. Miller, Assistant Secretary for Financial Markets. “We will exit this investment at a gradual and orderly pace to maximize the recovery of taxpayer dollars and help protect the process of repair of the housing finance market.”

The following frequently asked questions provide further information regarding Treasury’s plan to wind down its $142 billion portfolio of agency-guaranteed mortgage-backed securities (MBS) at a gradual and orderly pace. Starting this month, Treasury plans to sell up to $10 billion in agency-guaranteed MBS per month, subject to market conditions.

General

Why does Treasury hold a portfolio of agency-guaranteed MBS?

The Housing and Economic Recovery Act of 2008 (HERA) gave Treasury the authority to purchase agency-guaranteed MBS to provide stability to financial markets, prevent disruption in the availability of mortgage finance, and protect taxpayers. Treasury’s actions helped stabilize the mortgage market at a time of unprecedented market volatility and illiquidity. Treasury purchased agency-guaranteed MBS between October 2008 and December 2009. As of March 15, the current market value of Treasury’s holdings is approximately $142 billion.

Why is Treasury winding down its MBS portfolio?

Selling MBS is consistent with the general pattern of Treasury divestment of financial assets acquired during 2008 and 2009 as part of the various financial stabilization programs. Aided by such programs, today, the market for agency-guaranteed MBS has notably improved along with broader financial conditions since Treasury acquired the portfolio. Additionally, Treasury’s mission does not typically include managing a large mortgage portfolio.

When will the selling commence?

Treasury will begin to gradually wind down its MBS portfolio starting this month.

Over what time frame will the unwind take place?

Treasury plans to sell up to $10 billion of securities per month, subject to market conditions. This is in addition to principal payments (currently ranging between $3 and $5 billion per month). If the sales proceeded at the full $10 billion per month, the portfolio would be unwound in whole over approximately one year, depending on future rates of prepayments. If market conditions change and Treasury slows asset sales, it is possible that the unwind will take a longer period of time.

Once started, would Treasury consider suspending the sale of its MBS portfolio?

Selling the MBS portfolio is subject to market conditions. There is not a rigid set of criteria that will be used to suspend selling. Evidence of adverse market conditions could lead to a change in the sales frequency of the program. Treasury will constantly monitor the market, and if market conditions become less favorable, the sales could be suspended.

What impact will this program have on primary mortgage rates?

We believe that this portfolio can be sold with minimal impact on the market and a minimal impact on primary mortgage rates.

Under what authority is Treasury winding down its MBS portfolio?

The Housing and Economic Recovery Act of 2008 (HERA) gave Treasury the authority to sell holdings acquired under that act.

What implications will this approach have for Treasury debt issuance?

The sale of these securities will allow Treasury to borrow less in 2011 and 2012, but will not alter Treasury’s previously stated debt management objectives.

Is this action related to the debt limit?

No. This action is consistent with a general pattern of Treasury continued divestment of assets acquired during 2008 and 2009 as part of the various financial stabilization programs. Additionally, the projected pace of sales, $10 billion per month, will not meaningfully extend the expected time until Treasury will reach the debt limit.

Relationship to Housing Finance Reform and Fannie Mae and Freddie Mac (The “Enterprises”)

How does this announcement relate to the broader objectives of housing finance reform?

This action is independent from housing finance reform and is a part of the Administration’s broader efforts to wind down the emergency financial stabilization programs that were put in place in 2008 and 2009.

Will this announcement impact current administration policy regarding the wind down of the agency-guaranteed MBS held in the Enterprises’ portfolios?

No. The Enterprises are currently in the process of gradually reducing the size of their retained portfolios at a pace of no less than 10 percent per year, as they agreed to do in the preferred stock purchase agreements between the Treasury and the Enterprises. Both Enterprises are on track to meet or exceed the scheduled reductions, and the Administration does not anticipate any changes to this policy.

Will this announcement impact the Administration’s commitment to supporting the Enterprises’ obligations?

No. The government is committed to ensuring that Fannie Mae and Freddie Mac have sufficient capital to perform under any guarantees issued now or in the future and the ability to meet their debt obligations.

Execution Details

What types of MBS will be sold?

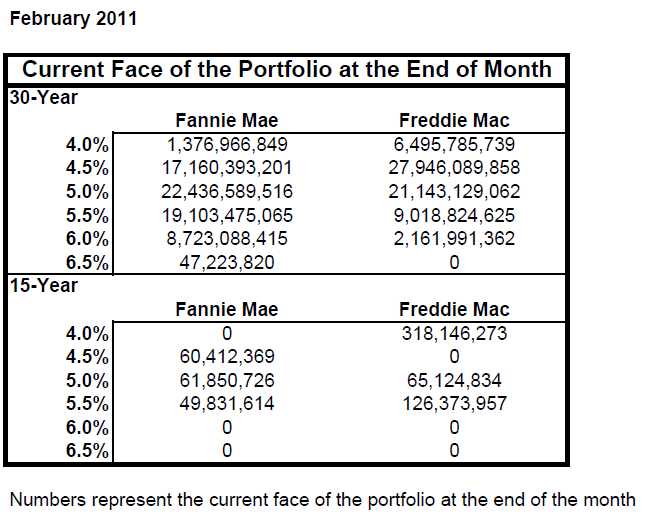

Treasury intends to sell all of its agency-guaranteed MBS holdings. Treasury’s portfolio consists primarily of 30-year fixed-rate MBS that are guaranteed by either Fannie Mae or Freddie Mac. There is also a smaller amount of 15-year fixed-rate MBS guaranteed by Fannie Mae and Freddie Mac, and one 10/20 MBS guaranteed by Fannie Mae. A complete list of the total MBS holdings by coupon and agency is available on the Treasury website at:

What will be the frequency of the sales?

There will be no pre-scheduled times and sizes of individual trades. Treasury will sell up to $10 billion per month, subject to market conditions. Sales of MBS out of the portfolio can occur daily.

How will you decide which securities to sell at any given time?

Treasury will monitor supply and demand dynamics in the market and determine the optimal timing for the sale of securities. Decisions to sell bonds will be based on both quantitative and qualitative market metrics. Treasury will also consider the composition of its portfolio holdings as well as indications of interest from eligible counterparties when determining security selection. State Street Global Advisors (SSgA) is the manager for Treasury’s portfolio and will assist in this analysis.

Will reverse inquiries be allowed?

Treasury will ensure a competitive bidding process that maximizes value for the taxpayer. Dealers are encouraged to show interest in specific trades or securities, but trades will be executed competitively.

Will these trades be specified pool trades or executed as “To-Be Announced” (TBA) trades?

Many of the securities in Treasury’s portfolio currently have a market value higher than TBA prices. As such, these securities will be traded as specified pools. Those securities that do not have a market value higher then TBA prices may be executed as TBA transactions.

Will the Treasury engage in coupon swaps and dollar rolls?

No. All transactions will be outright sales, as authorized by HERA.

Will you consider structuring Collateralized Mortgage Obligations (CMOs) as part of the unwind strategy?

No. Bonds will be sold as they were initially purchased without any additional structuring.

When will the trades settle?

Most trades will settle at monthly intervals on the regularly scheduled TBA settlement days. It is possible to settle trades on different days. Trades settling away from regularly scheduled TBA settlement days would only occur if they were in the taxpayers’ best interest.

Who will settle trades?

SSgA, as financial agent for the Treasury, will be responsible for facilitating the settlement of all sales in the portfolio.

Is the Treasury planning to reinvest the proceeds in any other assets?

No. As mandated under HERA and the Dodd-Frank Act, the proceeds from the MBS sales will be deposited in the General Fund of the Treasury.

Transparency

How will Treasury disclose completed sales?

Consistent with current practice, at the end of each month Treasury will post its portfolio holdings, including any sales that were completed, broken down by coupon and agency. That posting will be available on the Treasury website at: http://www.treasury.gov/resource-center/data-chart-center/Pages/mbs-purchase-program.aspx

Will Treasury post the exact CUSIPs that they own?

No. Given the Treasury’s approach to MBS sales, providing CUSIP level data could reduce the ability to efficiently execute sales.

Will Treasury provide a schedule in advance that displays the list of securities they intend to sell and times of transactions?

No. Treasury will retain flexibility to adjust to supply and demand conditions for specific issues and adjust its wind down strategy accordingly. This will provide the greatest opportunity to ensure best execution for the taxpayer through competitive sales.

Will you publish the counterparties in each MBS trade?

No. Treasury will not publish dealer market shares or specific trade details. Doing so would decrease the ability of Treasury to maximize value for taxpayers.

External Money Managers

Why is it necessary for the Treasury to transact through an external investment manager?

The operational characteristics of MBS purchases and sales are complex and external managers have an ability to execute and manage efficiently while, at the same time, minimizing operational and financial risks.

Treasury is not well positioned to actively trade mortgage-backed securities in the market on a day-to-day basis. External investment managers are used to ensure best execution in the market and maximize value for taxpayers.

How was SSgA selected?

SSgA was selected as part of a competitive process at the outset of the Treasury program to acquire, manage and dispose of MBS. Initially, Treasury hired both Barclays Global Investors (BGI) and SSgA. At the end of 2009, when Treasury completed its MBS purchases, administration of the program was consolidated and it is now managed solely by SSgA..

Is Treasury hiring other money managers to assist with security selection and execution strategy?

Yes. Smith, Graham, and Company Investment Advisors (Smith Graham) will provide additional assistance with the security selection process. On a weekly basis, Smith Graham will provide analytical support to Treasury.

Is Treasury considering hiring other money managers to assist with execution of the sales of MBS?

No. Adding additional managers would increase complexity and add to our operational risk. Intensive coordination and additional surveillance would be required to ensure that multiple independent managers did not work at cross purposes in the market. Using a single manager offers the best approach to optimizing the sale of the portfolio and protecting the taxpayers’ best interests.

How will Treasury ensure that SSgA is making prudent decisions on behalf of taxpayers?

In its agreement with Treasury, SSgA has a mandate to protect taxpayers and maximize value through best execution. Treasury will monitor SSgA and receive regular feedback regarding security selection, timing, and general market conditions to ensure that SSgA is fulfilling its obligations to taxpayers. Additionally, other divisions at SSgA will not be allowed to buy securities directly from Treasury’s portfolio.

What measures will Treasury take to ensure that SSgA will not have in unfair advantage relative to other market participants due to the information it receives?

A wall exists at SSgA that appropriately segregates the investment management team that implements the Treasury’s agency MBS program from other advisory trading activities of the firm. When Treasury hired SSgA, SSgA built a team that is focused exclusively on managing Treasury’s portfolio that is separate from the rest of the firm. Treasury monitors compliance with the requirement to maintain the wall.

Who will SSgA trade with?

SSgA will trade with dealers who meet SSgA’s counterparty credit requirements. Dealers may submit bids for themselves or on behalf of their clients.

Will SSgA be required to spread their business between dealers?

There are no pre-set market share targets for dealers. SSgA will ensure competition between dealers that maximizes best execution for the taxpayer. SSgA will also ensure diversity among the dealers. Treasury will constantly monitor the dealer selection process to ensure that no dealers or market participants are provided an unfair advantage.

FREQUENTLY ASKED QUESTIONS ON TREASURY’S PLAN TO SELL MBS

A few comments...

Treasury did not set a floor on how much MBS they can sell in a given month, but they did set a ceiling at $10 billion. If investor demand warrants, expect Treasury to offer $10 billion a month. If MBS valuations (yield spreads) weaken significantly as Treasury tries to sell, they will back off and let spreads stabilize before resuming operations. We don't expect that to happen unless benchmark yields rise substantially because, for example, the Fed hinted at a rate hike (4.5s would fall off a ledge). If necessary Treasury could halt this program all together, but $10 billion a month only adds $2.5 billion in loan supply per week. When you consider how slow a year it's been for new production MBS, we don't think it'll cause a major disruption.

In terms of timing, it would behoove Treasury to sell their lowest coupons first, especially if Treasury thinks rates will rise in the year ahead. At the moment Treasury is holding mostly 4.5 30-year coupons ($45 billion). With TBA supply very muted at the moment, we don't see many barriers that might prevent Treasury from selling the full $10 billion per month. If rates do drop substantially and the MBS market moves "Down in Coupon", Treasury may run into a barrier as investors look to avoid MBS coupons with heightened prepayment risk like 5.0s and 5.5s. Then again the street has been burned repeatedly over the past year by automatically assuming lower mortgage rates would equal a big jump in prepayment speeds. It just didn't happen. Qualifying for a loan isn't as simple as it used to be...one 30-day late is enough to kill a deal these days. Plus in the past, when prepayment speeds did pick up, investors looked for protection in the specified pool mortgage market. These MBS are backed by loans that have demonstrated a consistent performance (have a pay history). Generally MBS investors are willing to "pay-up" (pay more) to get their mitts on this paper. A large portion of Treasury's MBS holdings will be sold as specified "pay-ups". So even if rates do decline, there should still be demand for Treasury's holdings. (5.0 MBS coupons for example have already entered a "burnout" phase where lower rates will have little impact on prepayment speeds).

Plain and Simple: We don't see this causing a major disturbance in the TBA MBS market. The general direction of benchmark rates will largely dictate the direction of mortgage rates. We don't think this is a hint of things to come from the Fed either. When the Fed is ready to finally start selling their MBS holdings, the market will have already pushed rates higher and the market for their holdings would be weak because the coupons on their balance sheet would be trading at a sizeable discount. Thus the Fed will likely be forced to hold onto a large portion of their MBS portfolio to avoid shocking the market with too much duration.

The mortgage market was caught off-guard by this news though. Consequently there has been a knee-jerk reaction wider in current coupon MBS spreads and lower in current coupon MBS prices. That move has already started correcting though...

by Adam Quinones Mortgage News Daily March 21, 2011

Treasury to Sell MBS Holdings. Minimal Shock Expected

FDIC's Bair: Bank lending slowly opening up « HousingWire

Federal Deposit Insurance Corp. Chairman Sheila Bair said banks should look toward more lending even though financing via the securitization market is "not there anymore."

Bair spoke briefly Tuesday morning during a segment on CNBC's "Squawk on the Street," program.

"We want banks to lend to credit-worthy borrowers," Bair said. As the economy improves, Bair said she expects borrowers to commit to new business expansion and banks to be more willing to make loans. "Almost all indicators are for an improved banking sector," she added.

Bank closings peaked in 2010 at 157, up from 140 in 2009. Despite 25 closings already this year, Bair sees improvement on the horizon with significantly less bank failures expected this year.

Prudent lending, she said, will improve bank's earnings statements. "We are seeing a lot of improvement," Bair said, "credit quality is improving."

The FDIC's deposit insurance fund, meanwhile, is continuing to improve, she noted. Under the Dodd-Frank Act, the FDIC is required to set the designated reserve ratio at 2%. The rule took effect in January. Dodd-Frank gave the FDIC greater discretion to manage the DIF, including where to set the DRR. The financial reform law raises the minimum DRR, which the FDIC is required to set each year, to 1.35% from the former minimum of 1.15%. The FDIC has until Sept. 30, 2020, to get the fund reserve ratio up to 1.35%.

by Kerry Curry HousingWire March 22, 2011

FDIC's Bair: Bank lending slowly opening up « HousingWire

Bair spoke briefly Tuesday morning during a segment on CNBC's "Squawk on the Street," program.

"We want banks to lend to credit-worthy borrowers," Bair said. As the economy improves, Bair said she expects borrowers to commit to new business expansion and banks to be more willing to make loans. "Almost all indicators are for an improved banking sector," she added.

Bank closings peaked in 2010 at 157, up from 140 in 2009. Despite 25 closings already this year, Bair sees improvement on the horizon with significantly less bank failures expected this year.

Prudent lending, she said, will improve bank's earnings statements. "We are seeing a lot of improvement," Bair said, "credit quality is improving."

The FDIC's deposit insurance fund, meanwhile, is continuing to improve, she noted. Under the Dodd-Frank Act, the FDIC is required to set the designated reserve ratio at 2%. The rule took effect in January. Dodd-Frank gave the FDIC greater discretion to manage the DIF, including where to set the DRR. The financial reform law raises the minimum DRR, which the FDIC is required to set each year, to 1.35% from the former minimum of 1.15%. The FDIC has until Sept. 30, 2020, to get the fund reserve ratio up to 1.35%.

by Kerry Curry HousingWire March 22, 2011

FDIC's Bair: Bank lending slowly opening up « HousingWire

Saturday, March 19, 2011

G7 takes on the yen speculators - The Globe and Mail

The Group of Seven showed Friday that it still has the ability to bring global investors to heel, as its first co-ordinated intervention in foreign exchange markets in more than a decade stabilized the yen after several days of extreme volatility.

Japan's currency fell from Thursday's record, a relief to Japan's government as it struggles with a humanitarian disaster.

The G7’s clout, diminished in the past couple of years by the rise of the more inclusive Group of 20, will be tested when active trading resumes Monday. Markets in Japan will be closed for a holiday, but that won’t stop traders from buying yen elsewhere – if they dare.

After pushing the yen to a postwar high of 76.25 to the U.S. dollar, an appreciation that included a startling 4.3-per-cent gain in 10 minutes of trading Wednesday evening, investors backed down Friday in the face of concerted selling by central banks in Japan, Europe, the United States and Canada, a co-ordinated move aimed at holding down the currency of an economy already in deep trouble.

Many financial players were caught by surprise Friday, and David Watt, a senior currency strategist at RBC Dominion Securities in Toronto, predicts an uneasy stand-off on Monday.

“There are going to be a lot of people on the sidelines, with no one wanting to flinch and make the first move,” Mr. Watt said.

G7 authorities would prefer that everyone holster their weapons and walk away before there’s any more trouble. That could happen as investors reflect on the contradiction of a country in the midst of a historic crisis being saddled with one of the world's strongest currencies.

The yen appeared to accelerate on speculation that the Japanese will sell tens of billions of dollars in overseas assets to rebuild from last week’s earthquake and ensuing tsunami – a repatriation of funds that analysts say has yet to occur, and that is unlikely to happen to the degree suggested by the yen’s rise. The implication is that the surge was driven by speculators, rather thanJapanese insurance firms gathering yen for reconstruction.

Unlike its previous intervention in September, 2000, to prop up the euro, which was two years old and struggling to gain the confidence of traders, the G7 doesn’t appear to want to fundamentally change the value of the yen.

Until Wednesday’s sudden surge, the Japanese currency was trading fairly close to its historic average, Jens Nordvig, the New York-based global head of G10 currency strategy at Nomura Holdings Inc., said on a conference call Friday.

“There is no economic reason to live with a higher yen at such a dreadful time when it should be much lower,” said Wendy Dobson, co-director of the Institute for International Business at the University of Toronto’s Rotman School of Management and a former associate deputy minister in Canada’s Finance Department.

The G7’s intervention showed the group still has the resolve to rally to the aid of one of its own.

G7 members, the U.S., Japan, Germany, Britain, France, Italy and Canada, have been meeting as a group since the late 1970s under the auspices of steering the global economy. However, the financial crisis demonstrated that the world economy had become more than the postwar economic powers could control on their own. The G20, which includes emerging markets such as China, India and Brazil, was designated the primary body for co-ordinating economic policy at a summit of G20 leaders in Pittsburgh in 2009.

A stronger currency is a burden for Japan’s exporters at a time when the country’s economy can least afford it. The quake and ensuing tsunami killed thousands, and the destruction has disrupted production at companies such as Toyota Corp. and Sony Corp. The country remains on edge as authorities struggle to contain radiation leaks at a shattered nuclear plant.

"A targeted strategy to take some of the pressure off the yen in Japan’s time of exceptional need is a great example of how macro policy co-ordination among the major economies can make a positive difference,” said Glen Hodgson, chief economist at the Conference Board of Canada in Ottawa and a former official at Canada’s Finance Department.

In a statement after the meeting via conference call on Thursday evening, G7 finance ministers and central bankers said they were ready to “provide any needed co-operation” as Japan rebuilds.

But the statement also hinted at concern that this week’s unusual trading in the yen risked triggering a broader crisis in international markets. “As we have long stated, excess volatility and disorderly movements in exchange rates have adverse implications for economic and financial stability,” officials said. “We will monitor exchange markets closely and will co-operate as appropriate.”

That suggests the trigger for further action will be a sudden jump from what officials consider fair value of the Japanese currency. Many analysts reckon the G7’s central banks will hold their fire as long as the yen holds a value of around 80 to the U.S. dollar.

“Above all, the G7’s role was an attempt to stabilize markets,” Camilla Sutton, chief currency strategist at Scotia Capital in Toronto, said in a research note Friday. “Any further disorderly movements in (the dollar-yen rate) will likely be met with renewed commitment from the G7.”

The Bank of Japan led the action, exchanging some ¥2-trillion for dollars, a transaction worth about $25-billion (U.S.), Bloomberg News reported, citing a Japanese official. The European Central Bank, the Bank of France, Germany’s Bundesbank, and the Bank of Italy followed as markets opened in Europe, selling yen to weaken the Japanese currency’s value. The Federal Reserve and the Bank of Canada did the same as trading began in North America.

Central banks in Europe and North America declined to reveal the scale of their yen sales. Currency analysts estimated their contributions were largely symbolic – the equivalent of a shot across the bow to show traders that their monetary authorities are watching.

In September, Japan intervened unilaterally to weaken the yen after the currency had strengthened at that point to about 83 to the dollar, a decision that drew scorn from European officials, who accused the Japanese government of seeking an advantage for its exporters.

The Bank of Japan sold ¥2-trillion in that effort and then backed down. Japanese authorities will have a better chance of fighting currency traders with the backing of the G7, analysts said.

“It’s very important to remember what happened in September,” Mr. Nordvig said. The Japanese government now has “the clear backing of the G7,” he said. “It makes the operation that much more likely to have a permanent impact.”

by Kevin Carmichael The Globe and Mail March 18, 2011

G7 takes on the yen speculators - The Globe and Mail

Japan's currency fell from Thursday's record, a relief to Japan's government as it struggles with a humanitarian disaster.

The G7’s clout, diminished in the past couple of years by the rise of the more inclusive Group of 20, will be tested when active trading resumes Monday. Markets in Japan will be closed for a holiday, but that won’t stop traders from buying yen elsewhere – if they dare.

After pushing the yen to a postwar high of 76.25 to the U.S. dollar, an appreciation that included a startling 4.3-per-cent gain in 10 minutes of trading Wednesday evening, investors backed down Friday in the face of concerted selling by central banks in Japan, Europe, the United States and Canada, a co-ordinated move aimed at holding down the currency of an economy already in deep trouble.

Many financial players were caught by surprise Friday, and David Watt, a senior currency strategist at RBC Dominion Securities in Toronto, predicts an uneasy stand-off on Monday.

“There are going to be a lot of people on the sidelines, with no one wanting to flinch and make the first move,” Mr. Watt said.

G7 authorities would prefer that everyone holster their weapons and walk away before there’s any more trouble. That could happen as investors reflect on the contradiction of a country in the midst of a historic crisis being saddled with one of the world's strongest currencies.

The yen appeared to accelerate on speculation that the Japanese will sell tens of billions of dollars in overseas assets to rebuild from last week’s earthquake and ensuing tsunami – a repatriation of funds that analysts say has yet to occur, and that is unlikely to happen to the degree suggested by the yen’s rise. The implication is that the surge was driven by speculators, rather thanJapanese insurance firms gathering yen for reconstruction.

Unlike its previous intervention in September, 2000, to prop up the euro, which was two years old and struggling to gain the confidence of traders, the G7 doesn’t appear to want to fundamentally change the value of the yen.

Until Wednesday’s sudden surge, the Japanese currency was trading fairly close to its historic average, Jens Nordvig, the New York-based global head of G10 currency strategy at Nomura Holdings Inc., said on a conference call Friday.

“There is no economic reason to live with a higher yen at such a dreadful time when it should be much lower,” said Wendy Dobson, co-director of the Institute for International Business at the University of Toronto’s Rotman School of Management and a former associate deputy minister in Canada’s Finance Department.

The G7’s intervention showed the group still has the resolve to rally to the aid of one of its own.

G7 members, the U.S., Japan, Germany, Britain, France, Italy and Canada, have been meeting as a group since the late 1970s under the auspices of steering the global economy. However, the financial crisis demonstrated that the world economy had become more than the postwar economic powers could control on their own. The G20, which includes emerging markets such as China, India and Brazil, was designated the primary body for co-ordinating economic policy at a summit of G20 leaders in Pittsburgh in 2009.

A stronger currency is a burden for Japan’s exporters at a time when the country’s economy can least afford it. The quake and ensuing tsunami killed thousands, and the destruction has disrupted production at companies such as Toyota Corp. and Sony Corp. The country remains on edge as authorities struggle to contain radiation leaks at a shattered nuclear plant.

"A targeted strategy to take some of the pressure off the yen in Japan’s time of exceptional need is a great example of how macro policy co-ordination among the major economies can make a positive difference,” said Glen Hodgson, chief economist at the Conference Board of Canada in Ottawa and a former official at Canada’s Finance Department.

In a statement after the meeting via conference call on Thursday evening, G7 finance ministers and central bankers said they were ready to “provide any needed co-operation” as Japan rebuilds.

But the statement also hinted at concern that this week’s unusual trading in the yen risked triggering a broader crisis in international markets. “As we have long stated, excess volatility and disorderly movements in exchange rates have adverse implications for economic and financial stability,” officials said. “We will monitor exchange markets closely and will co-operate as appropriate.”

That suggests the trigger for further action will be a sudden jump from what officials consider fair value of the Japanese currency. Many analysts reckon the G7’s central banks will hold their fire as long as the yen holds a value of around 80 to the U.S. dollar.

“Above all, the G7’s role was an attempt to stabilize markets,” Camilla Sutton, chief currency strategist at Scotia Capital in Toronto, said in a research note Friday. “Any further disorderly movements in (the dollar-yen rate) will likely be met with renewed commitment from the G7.”

The Bank of Japan led the action, exchanging some ¥2-trillion for dollars, a transaction worth about $25-billion (U.S.), Bloomberg News reported, citing a Japanese official. The European Central Bank, the Bank of France, Germany’s Bundesbank, and the Bank of Italy followed as markets opened in Europe, selling yen to weaken the Japanese currency’s value. The Federal Reserve and the Bank of Canada did the same as trading began in North America.

Central banks in Europe and North America declined to reveal the scale of their yen sales. Currency analysts estimated their contributions were largely symbolic – the equivalent of a shot across the bow to show traders that their monetary authorities are watching.

In September, Japan intervened unilaterally to weaken the yen after the currency had strengthened at that point to about 83 to the dollar, a decision that drew scorn from European officials, who accused the Japanese government of seeking an advantage for its exporters.

The Bank of Japan sold ¥2-trillion in that effort and then backed down. Japanese authorities will have a better chance of fighting currency traders with the backing of the G7, analysts said.

“It’s very important to remember what happened in September,” Mr. Nordvig said. The Japanese government now has “the clear backing of the G7,” he said. “It makes the operation that much more likely to have a permanent impact.”

by Kevin Carmichael The Globe and Mail March 18, 2011

G7 takes on the yen speculators - The Globe and Mail

Housing-vacancy rates high in outlying Valley

Metro Phoenix population and housing data from the U.S. Census Bureau shows which cities in the region experienced the most overbuilding during the mid-decade boom. It also shows which areas have the lowest vacancy rates or number of vacant homes.

Many of the region's edge communities experienced big increases in population, but homebuilding still outpaced new residents. Buckeye's population climbed by 678 percent, but the city's number of housing units climbed even more. So now, it has a 21 percent vacancy rate.

Some other Phoenix-area cities with higher-than-average housing vacancies: Apache Junction, 31 percent; Scottsdale, 18.3 percent; and Surprise, 17.7 percent.

Arizona's overall housing-vacancy rate is 15.6 percent.

Three southeast Valley communities posted lower-than-average housing vacancies: Tempe, 10.2 percent; Chandler, 7.9 percent; and Gilbert, 7.4 percent.

Phoenix's housing-vacancy rate is 12.8 percent.

Some Arizona cities with many second-home owners, including Scottsdale and Apache Junction, have housing vacancies that look high to market watchers. Data to be released later this year for Arizona will give those second-home hubs better counts.

More than half underwater

As many as 51 percent of Arizona homeowners are underwater, according to new data from CoreLogic. Nevada has the highest rate of homeowners owing more than their house is worth, at 65 percent. Florida is right behind Arizona, with 47 percent of its homeowners dealing with negative equity.

The national rate for negative equity is 23 percent.

Arizona's rate has actually dropped as more homeowners have lost houses to foreclosure. That means fewer people owe more on a mortgage than their house is worth.

Refinancing aid

The federal Home Affordable Refinancing Program, better known as HARP, has been extended for another year. The program was due to expire at the end of June but was extended despite congressional debates on killing the Home Affordable Modification Program because it has helped fewer than expected.

HARP helps homeowners who owe more than their house is worth to refinance but is limited to 125 percent loan-to-value, so many prospective borrowers in metro Phoenix don't qualify.

by Catherine Reagor The Arizona Republic Mar. 16, 2011 12:00 AM

Housing-vacancy rates high in outlying Valley

Many of the region's edge communities experienced big increases in population, but homebuilding still outpaced new residents. Buckeye's population climbed by 678 percent, but the city's number of housing units climbed even more. So now, it has a 21 percent vacancy rate.

Some other Phoenix-area cities with higher-than-average housing vacancies: Apache Junction, 31 percent; Scottsdale, 18.3 percent; and Surprise, 17.7 percent.

Arizona's overall housing-vacancy rate is 15.6 percent.

Three southeast Valley communities posted lower-than-average housing vacancies: Tempe, 10.2 percent; Chandler, 7.9 percent; and Gilbert, 7.4 percent.

Phoenix's housing-vacancy rate is 12.8 percent.

Some Arizona cities with many second-home owners, including Scottsdale and Apache Junction, have housing vacancies that look high to market watchers. Data to be released later this year for Arizona will give those second-home hubs better counts.

More than half underwater

As many as 51 percent of Arizona homeowners are underwater, according to new data from CoreLogic. Nevada has the highest rate of homeowners owing more than their house is worth, at 65 percent. Florida is right behind Arizona, with 47 percent of its homeowners dealing with negative equity.

The national rate for negative equity is 23 percent.

Arizona's rate has actually dropped as more homeowners have lost houses to foreclosure. That means fewer people owe more on a mortgage than their house is worth.

Refinancing aid

The federal Home Affordable Refinancing Program, better known as HARP, has been extended for another year. The program was due to expire at the end of June but was extended despite congressional debates on killing the Home Affordable Modification Program because it has helped fewer than expected.

HARP helps homeowners who owe more than their house is worth to refinance but is limited to 125 percent loan-to-value, so many prospective borrowers in metro Phoenix don't qualify.

by Catherine Reagor The Arizona Republic Mar. 16, 2011 12:00 AM

Housing-vacancy rates high in outlying Valley

FBI raids Scottsdale financial firm

A hard-money lending firm specializing in commercial real estate was shut down for several hours on Tuesday after the FBI served it with a sealed search warrant.

Some employees of Remington Capital Inc. of Scottsdale were at times sequestered in the firm's lobby while roughly a dozen FBI agents, some in bulletproof vests, collected company records and documents as evidence. Its headquarters is on Raintree Drive east of Loop 101 in the Raintree Corporate Center.

The premise for the warrant was unavailable and will remain so until the document is unsealed by a federal judge, said Brenda Nath, an FBI spokeswoman. "We can't give any other information," Nath said.

She said the warrant does not necessarily mean that the firm is or will be under federal investigation.

Hard-money lending firms offer alternative financing options, at much higher interest rates and service fees, to projects in which traditional financial institutions deem too risky to invest. Such firms have been under scrutiny since the real-estate crash a few years ago.

A spokeswoman for the office of Arizona Attorney General Tom Horne said the agency was unable to disclose whether staff members were investigating Remington. Jon Hamel of Cavan Property Management said Remington Capital has been a tenant for about a year.

Company officials were unavailable for comment.

In Arizona Corporation Commission records, Andrew Bogdanoff is listed as the president of Remington Capital Inc., which was founded in 1993 and specializes in securing domestic and international commercial-real-estate financing for its clients.

Other Remington executives listed on its website include Shayne Fowler, chief operating officer and managing partner; Donavon Ostrom, head of Remington's Capital Markets Group; and Tyler Hufford, managing director of operations.

Bogdanoff was listed as the owner of Remington Financial Group Inc., which also lists the Raintree Corporate Center as its office location on its website.

In 2008, Remington Financial and a related firm, BlueStone Real Estate Capital, were reported by the Wall Street Journal to be under investigation by the FBI and securities regulators in California and Philadelphia to determine whether the firms were accepting service fees without trying to obtain financing for its clients.

Remington also was a defendant in six lawsuits in California Superior Court involving similar accusations, the article said.

No updated information could be immediately found in court records or media reports. Remington denied the accusations, according to the Journal. The firm also has taken a public stance against fraud.

In May 2010, Bogdanoff was cited in a Remington Financial news release that he had alerted the FBI and other agencies that an Internet scam was using his name to obtain information that could be used in ID theft. On Feb. 25, the company changed its name to Remington Capital.

Don Gaffney of Snell & Wilmer in Phoenix represented one of the plaintiffs in a lawsuit against hard-money lender firm Mortgages Ltd. a few years ago. Generally, problems arise when there are issues with liquidity, he said.

by Kristena Hansen The Arizona Republic Mar. 16, 2011 12:00 AM

FBI raids Scottsdale financial firm

Some employees of Remington Capital Inc. of Scottsdale were at times sequestered in the firm's lobby while roughly a dozen FBI agents, some in bulletproof vests, collected company records and documents as evidence. Its headquarters is on Raintree Drive east of Loop 101 in the Raintree Corporate Center.

The premise for the warrant was unavailable and will remain so until the document is unsealed by a federal judge, said Brenda Nath, an FBI spokeswoman. "We can't give any other information," Nath said.

She said the warrant does not necessarily mean that the firm is or will be under federal investigation.

Hard-money lending firms offer alternative financing options, at much higher interest rates and service fees, to projects in which traditional financial institutions deem too risky to invest. Such firms have been under scrutiny since the real-estate crash a few years ago.

A spokeswoman for the office of Arizona Attorney General Tom Horne said the agency was unable to disclose whether staff members were investigating Remington. Jon Hamel of Cavan Property Management said Remington Capital has been a tenant for about a year.

Company officials were unavailable for comment.

In Arizona Corporation Commission records, Andrew Bogdanoff is listed as the president of Remington Capital Inc., which was founded in 1993 and specializes in securing domestic and international commercial-real-estate financing for its clients.

Other Remington executives listed on its website include Shayne Fowler, chief operating officer and managing partner; Donavon Ostrom, head of Remington's Capital Markets Group; and Tyler Hufford, managing director of operations.

Bogdanoff was listed as the owner of Remington Financial Group Inc., which also lists the Raintree Corporate Center as its office location on its website.

In 2008, Remington Financial and a related firm, BlueStone Real Estate Capital, were reported by the Wall Street Journal to be under investigation by the FBI and securities regulators in California and Philadelphia to determine whether the firms were accepting service fees without trying to obtain financing for its clients.

Remington also was a defendant in six lawsuits in California Superior Court involving similar accusations, the article said.

No updated information could be immediately found in court records or media reports. Remington denied the accusations, according to the Journal. The firm also has taken a public stance against fraud.

In May 2010, Bogdanoff was cited in a Remington Financial news release that he had alerted the FBI and other agencies that an Internet scam was using his name to obtain information that could be used in ID theft. On Feb. 25, the company changed its name to Remington Capital.

Don Gaffney of Snell & Wilmer in Phoenix represented one of the plaintiffs in a lawsuit against hard-money lender firm Mortgages Ltd. a few years ago. Generally, problems arise when there are issues with liquidity, he said.

by Kristena Hansen The Arizona Republic Mar. 16, 2011 12:00 AM

FBI raids Scottsdale financial firm

Group pushes construction boost

Citing a job crisis in the construction sector, a national trade group that represents general contractors met Tuesday in Phoenix to urge state and federal officials to take steps to help revive the industry.

Leaders of the Virginia-based Associated General Contractors of America held a news conference Tuesday morning in front of the stalled Hotel Monroe project, 15 E. Monroe St.

The group's CEO, Stephen Sandherr, said his organization chose Phoenix as the site where it would announce its list of job-boosting recommendations because metro Phoenix has lost the most construction jobs in the current economic downturn.

Sandherr said Phoenix has lost more than 91,000 full-time construction jobs during the four years that ended in January. That's more than half of the roughly 170,000 workers employed in January 2007.

"Looking at a project like this, it's easy to understand why the construction industry is still in a recession," Sandherr said about the boarded-up Hotel Monroe, one of the failed projects funded by the now-defunct Scottsdale investment broker and construction lender Mortgages Ltd.

Sandherr said the unemployment rate in his industry is 21.8 percent, noting that the lack of construction jobs has ripple effects that hinder the country's overall economic recovery.

With that in mind, the trade group issued a list of recommendations that Sandherr said would give the construction industry a needed boost.

They included an increase in federal spending on public-infrastructure projects. The federal government spent about $135 billion in 2009 and 2010 in economic-stimulus funds on construction projects, but most of the projects have been completed and are no longer a source of work for construction firms.

Sandherr called for Congress to make permanent President George W. Bush's tax cuts of 2001 and 2003, which apply to income taxes on small businesses and individuals earning more than $250,000 a year.

Congress recently renewed the tax cuts for two years, but the Obama administration has said it doesn't want them to be made permanent.

The group also wants reforms that would reduce taxes on construction projects and companies, including the expansion of "loss-carryback" tax rules, which allow companies currently operating at a loss to obtain refunds on tax payments made during profitable years.

In addition, it called for a revival of the expired Build America Bonds program, in which the federal government subsidized 35 percent of the interest payments on public construction projects.

The group's other recommendations included lifting federal trade restrictions that discourage manufacturing in the U.S., easing U.S. Environmental Protection Agency regulation of construction projects, encouraging public-private partnerships with tax breaks, revenue subsidies or other measures, and accelerating projects aimed at providing the country with cleaner and more renewable energy, such as by fast-tracking the licensing of new nuclear plants.

by J. Craig Anderson The Arizona Republic Mar. 16, 2011 12:00 AM

Group pushes construction boost

Leaders of the Virginia-based Associated General Contractors of America held a news conference Tuesday morning in front of the stalled Hotel Monroe project, 15 E. Monroe St.

The group's CEO, Stephen Sandherr, said his organization chose Phoenix as the site where it would announce its list of job-boosting recommendations because metro Phoenix has lost the most construction jobs in the current economic downturn.

Sandherr said Phoenix has lost more than 91,000 full-time construction jobs during the four years that ended in January. That's more than half of the roughly 170,000 workers employed in January 2007.

"Looking at a project like this, it's easy to understand why the construction industry is still in a recession," Sandherr said about the boarded-up Hotel Monroe, one of the failed projects funded by the now-defunct Scottsdale investment broker and construction lender Mortgages Ltd.

Sandherr said the unemployment rate in his industry is 21.8 percent, noting that the lack of construction jobs has ripple effects that hinder the country's overall economic recovery.

With that in mind, the trade group issued a list of recommendations that Sandherr said would give the construction industry a needed boost.

They included an increase in federal spending on public-infrastructure projects. The federal government spent about $135 billion in 2009 and 2010 in economic-stimulus funds on construction projects, but most of the projects have been completed and are no longer a source of work for construction firms.

Sandherr called for Congress to make permanent President George W. Bush's tax cuts of 2001 and 2003, which apply to income taxes on small businesses and individuals earning more than $250,000 a year.

Congress recently renewed the tax cuts for two years, but the Obama administration has said it doesn't want them to be made permanent.

The group also wants reforms that would reduce taxes on construction projects and companies, including the expansion of "loss-carryback" tax rules, which allow companies currently operating at a loss to obtain refunds on tax payments made during profitable years.

In addition, it called for a revival of the expired Build America Bonds program, in which the federal government subsidized 35 percent of the interest payments on public construction projects.

The group's other recommendations included lifting federal trade restrictions that discourage manufacturing in the U.S., easing U.S. Environmental Protection Agency regulation of construction projects, encouraging public-private partnerships with tax breaks, revenue subsidies or other measures, and accelerating projects aimed at providing the country with cleaner and more renewable energy, such as by fast-tracking the licensing of new nuclear plants.

by J. Craig Anderson The Arizona Republic Mar. 16, 2011 12:00 AM

Group pushes construction boost

New Arizona mortgage-aid plan: Investors lend to owners

Some Arizona homeowners under water on their mortgages might be able to reduce their interest rates and monthly payments if a proposed state program becomes law.

The "home certificate" program laid out in a new bill is intended to help homeowners lower their mortgage payments even if they can't refinance their mortgages through a traditional bank.

The proposal is both unprecedented and controversial. Essentially, it would create a separate market for mortgage financing from private investors, bypassing banks. Investors could benefit by earning interest paid by reliable borrowers, while homeowners could benefit from lower monthly payments and lower interest rates than they currently have.

Although the plan's backer says it could help many homeowners, critics say lenders will be reluctant to agree to the system.

Roadblocks

The program, which is intended to be short-term, might also put borrowers at risk and won't work if home values don't rebound enough for borrowers to refinance later, letting investors get back the money they put in.

Since the crash in home values, many Valley residents now owe more on their mortgages than their homes are worth. In that situation, they typically can't qualify to refinance. Their homes aren't worth enough for lenders to issue them a new mortgage at a lower interest rate.

That situation leaves homeowners, even those with good credit who can make their payments, unable to take advantage of lower interest rates.

Those are the homeowners the bill aims to help.

The legislation, backed by Scottsdale Republican Sen. Michelle Reagan, has passed the Senate and has been assigned to be heard in the House Commerce Committee, but that hearing is not yet scheduled.

Reagan said she believes the bill can help responsible homeowners unable to refinance to current low interest rates and set up a system for investors to make money.

"It's a private program that is based on free-market principles," Reagan said.

How it works

The system would work this way:

- Arizona homeowners would qualify if they were current on their mortgage payments but owed more than their houses were worth.

- Qualifying homeowners would enter a marketplace managed by a state agency that has not yet been designated. They would publicly post the monthly payment they were willing to make - typically a payment lower than their current bill and equivalent to their current mortgage but with an interest rate of 2 to 5 percent.

- Investors would evaluate those mortgage requests and then bid on the loans they wanted to buy.

- When investors and borrowers were matched up, the investors would pay off the homeowners' old loans. Homeowners then could make payments, at a lower interest rate, to the investors. Investors would make 2 to 5 percent interest, which Reagan noted is more than they can currently earn by saving cash in a bank.

- Borrowers would have to sign away their "anti-deficiency" rights. Laws in Arizona say banks in most cases cannot pursue homeowners to recoup any losses after foreclosing on a home. Waiving anti-deficiency rights is meant to reassure investors that borrowers wouldn't abandon their homes without repaying.