The U.S.'s economic recovery looks a bit bottom-heavy - it been dominated by the return of lower-wage jobs.

That's the assessment of the National Employment Law Project in a report released last week.

While more than 1 million private-sector jobs were added to the U.S. economy during the past year, they have been concentrated in mid- and low-wage industries, the project concluded.

"This snapshot suggests that the job opportunities currently available to workers have deteriorated compared to what was available before the recession," said Annette Bernhardt, policy co-director for the project. "If these trends continue, the slow recovery combined with imbalanced growth could make it much harder for workers to find family-supporting jobs and pose real obstacles to restoring consumer demand."

A disproportionate share of job growth has been in industries such as temporary employment services, restaurants, retail, and nursing and residential-care facilities, which pay median wages below $13 an hour, the organization reported.

The study also found: Lower-wage industries constituted 23 percent of job loss but 49 percent of recent growth; midwage industries constituted 36 percent of job loss and 37 percent of recent growth; and higher-wage industries constituted 40 percent of job loss but only 14 percent of recent growth.

While it is unclear if these early figures represent a long-term trend, Bernhardt said they "underscore the urgent need

by Jahna Berry The Arizona Republic Feb. 27, 2011 12:00 AM

Low-wage jobs lead economic recovery

Sunday, February 27, 2011

Tips for transferring a credit-card balance

NEW YORK - Don't like the terms on your credit card? It could be time to take your business elsewhere.

Balance-transfer offers are getting a whole lot sweeter for those with good to excellent credit. Introductory rates of 0 percent are now as long as 18 months, more than double the average time offered at the height of the recession.

The newfound generosity comes as banks compete to land the top spenders with clean credit records. These customers are increasingly prized now that new regulations have limited the penalty charges issuers can collect from less reliable cardholders.

Before jumping at the chance to switch cards, however, there are pros and cons that need to be weighed carefully. For example, it might turn out the introductory rate isn't worth the transfer fees or a higher regular rate that kicks in later. Moving your balance to another card could also ding your credit score.

Here's what you should know before making the leap:

The fees

It's intended to catch your eye - "0 percent introductory rate!" What isn't so prominently advertised is the fee you'll be charged for moving your balance.

This fee is typically 3 to 5 percent of your balance. And unlike before the recession, most issuers no longer cap how high that fee can go. So on a $10,000 balance, the fee would be between $300 and $500.

To properly size up the value of any balance transfer offer, you'll need to weigh the fee against any potential savings on interest charges. Luckily, the proliferation of online credit-card calculators means you don't have to put your math skills to the test.

Bankrate.com has a detailed balance-transfer calculator that can be found at tinyurl.com/6ceebrg. For a simpler version that looks solely at potential interest costs, try CardHub.com's calculator at tinyurl.com/6ao4n3u.

Remember that you need to be realistic about how quickly you intend to pay off your balance. Otherwise, your estimates on how much you stand to save will be way off base.

Rates and rewards

A 0 percent introductory rate on balance transfers is standard. The key is looking at the terms you'll face once the honeymoon ends.

To start, check the regular interest rate that takes effect after the introductory period. The offer will cite a range of rates; the exact rate you're approved for will depend on your credit profile. And don't forget that a late payment could trigger that interest rate earlier.

Also be aware that the interest rate on balance transfers doesn't always apply to new purchases during the introductory period. Or you may get 0 percent interest on new purchases for a shorter period than for your balance transfer.

You also want to evaluate any tradeoffs you'll be making in the rewards department.

To compare the different offers on the market, go to Bankrate.com, CardHub.com or CreditCards.com. It's also worth calling your issuer to see what offers are available.

Repercussions

Beyond the more obvious costs and savings, you'll also want to consider the impact a balance transfer could have on your credit score.

If you have strong credit, the impact of a balance transfer is usually minimal over time. But if you're planning on applying for a mortgage or other big loan in the near future, there are some issues to keep in mind.

Applying for a new card dings your credit score in the short term because it suggests you're in need of money. Your credit score can also take hits when an account is closed. This is in part because closing an account lowers your total credit line. A smaller component in your score is the length of your credit history. So you want to think twice before closing one of your oldest accounts.

If you're tempted by a balance-transfer offer but worried about hurting your score, see if you can use the offer to negotiate for better terms on your current card.

Even if you have a spotless payment record, however, don't expect to receive a matching offer of 0 percent for 12 months, said Ben Woolsey, director of consumer research at CreditCards.com

"The most you can expect is a reduction in your interest rate," Woolsey said.

In many cases, that may be all you were hoping for.

by Candice Choi Associated Press Feb. 27, 2011 12:00 AM

Tips for transferring a credit-card balance

Balance-transfer offers are getting a whole lot sweeter for those with good to excellent credit. Introductory rates of 0 percent are now as long as 18 months, more than double the average time offered at the height of the recession.

The newfound generosity comes as banks compete to land the top spenders with clean credit records. These customers are increasingly prized now that new regulations have limited the penalty charges issuers can collect from less reliable cardholders.

Before jumping at the chance to switch cards, however, there are pros and cons that need to be weighed carefully. For example, it might turn out the introductory rate isn't worth the transfer fees or a higher regular rate that kicks in later. Moving your balance to another card could also ding your credit score.

Here's what you should know before making the leap:

The fees

It's intended to catch your eye - "0 percent introductory rate!" What isn't so prominently advertised is the fee you'll be charged for moving your balance.

This fee is typically 3 to 5 percent of your balance. And unlike before the recession, most issuers no longer cap how high that fee can go. So on a $10,000 balance, the fee would be between $300 and $500.

To properly size up the value of any balance transfer offer, you'll need to weigh the fee against any potential savings on interest charges. Luckily, the proliferation of online credit-card calculators means you don't have to put your math skills to the test.

Bankrate.com has a detailed balance-transfer calculator that can be found at tinyurl.com/6ceebrg. For a simpler version that looks solely at potential interest costs, try CardHub.com's calculator at tinyurl.com/6ao4n3u.

Remember that you need to be realistic about how quickly you intend to pay off your balance. Otherwise, your estimates on how much you stand to save will be way off base.

Rates and rewards

A 0 percent introductory rate on balance transfers is standard. The key is looking at the terms you'll face once the honeymoon ends.

To start, check the regular interest rate that takes effect after the introductory period. The offer will cite a range of rates; the exact rate you're approved for will depend on your credit profile. And don't forget that a late payment could trigger that interest rate earlier.

Also be aware that the interest rate on balance transfers doesn't always apply to new purchases during the introductory period. Or you may get 0 percent interest on new purchases for a shorter period than for your balance transfer.

You also want to evaluate any tradeoffs you'll be making in the rewards department.

To compare the different offers on the market, go to Bankrate.com, CardHub.com or CreditCards.com. It's also worth calling your issuer to see what offers are available.

Repercussions

Beyond the more obvious costs and savings, you'll also want to consider the impact a balance transfer could have on your credit score.

If you have strong credit, the impact of a balance transfer is usually minimal over time. But if you're planning on applying for a mortgage or other big loan in the near future, there are some issues to keep in mind.

Applying for a new card dings your credit score in the short term because it suggests you're in need of money. Your credit score can also take hits when an account is closed. This is in part because closing an account lowers your total credit line. A smaller component in your score is the length of your credit history. So you want to think twice before closing one of your oldest accounts.

If you're tempted by a balance-transfer offer but worried about hurting your score, see if you can use the offer to negotiate for better terms on your current card.

Even if you have a spotless payment record, however, don't expect to receive a matching offer of 0 percent for 12 months, said Ben Woolsey, director of consumer research at CreditCards.com

"The most you can expect is a reduction in your interest rate," Woolsey said.

In many cases, that may be all you were hoping for.

by Candice Choi Associated Press Feb. 27, 2011 12:00 AM

Tips for transferring a credit-card balance

Sectors spar over fee cap on debit use

Americans now make more than one-third of their purchases using debit cards, and all those swipes of the plastic have provoked a nasty battle.

The fighting between the retail and financial industrials is over interchange fees on debit transactions. After years of merchant complaints, Congress in December instructed the Federal Reserve to cut the fees to 12 cents per swipe, down from an estimate of 44 cents or higher, depending on whom you talk to. Regardless, the change adds up to billions of dollars.

Merchants have been griping that these fees cut into their already-thin profit margins and prevent them from passing along lower prices to consumers.

Banks, credit unions and card issuers say the fees pay to implement and operate their debit systems and help absorb fraud costs.

Consumers don't foot the costs directly, although some merchants add surcharges, and many others are vocal about the costs they absorb. But consumers will be affected by how this debate plays out.

The Fed's fee cap is set to be adopted by April 21 and take effect three months later. The financial industry, with sympathy from some members of Congress, is seeking a delay.

Retailer groups call the current system anti-competitive. They say it allows Visa and MasterCard to fix swipe fees with no opportunity for bargaining or competition. They say swipe fees have tripled over the past decade even as bank costs have decreased.

"Rates have gone up unchecked for the last 10 years," said Tim McCabe, president of the Arizona Food Marketing Alliance, which represents 1,400 supermarkets, convenience stores and other retailers.

"As technology has advanced and we have gotten away from paper, you'd expect these fees to decrease, but they haven't."

The Merchants Payments Coalition, a national group of which the Arizona Food Marketing Alliance is a member, estimates the cap will generate $13 billion in annual savings for merchants and consumers.

Retailers have accused big banks of "scare tactics" to rally small banks and credit unions to their side.

The proposal does provide a fee-cap exemption for smaller banks and credit unions - those with assets below $10 billion. But it doesn't require that debit-payment networks distinguish between the two.

The Fed has solicited comments for the past two months, and Congress has held hearings, so it's possible the new rules could be altered or delayed.

"Quite frankly, some small issuers are concerned networks may not provide a two-tiered structure once the rule is final or may not maintain it into the future," said Mary Mitchell Dunn, a senior vice president at the Credit Union National Association, in a recent letter to the Fed.

"Without a two-tiered structure, there is no exemption."

CUNA and the 70 percent of credit unions that offer debit are "extremely concerned about the impact of this proposal on their members, their debit-card programs and their operations generally," she wrote.

Credit unions can't pass the buck to shareholders - because they don't have any. Instead, their members would feel the pain through increased fees for various services or lower interest rates paid on deposits.

CUNA estimates credit-union debit customers could face an average new annual fee of $34, a transaction fee of 25 cents per swipe or some combination.

Paul Stull, a vice president at Arizona State Credit Union, estimates the proposed fee cap would cost his institution more than $5 million annually.

"In the end, our members would pay higher fees or will have reduced services," he said.

Swipe fees also help banks and credit unions absorb fraud losses, including those caused by a merchant's failure to check identifications or otherwise validate purchases.

Stull cited a recent case in which crooks installed card-reading skimmers at Tucson-area gas stations and used the cardholder information they obtained to make fake ATM cards, employing those to extract illicit withdrawals.

"Our losses from that came to more than $10,000 within a few days," he said. "But the gas stations got all their money, and our members didn't lose any money."

Small community banks, which have been hit much harder than their large counterparts by the soft economy, also are worried.

"A lot of people look at it as a big-bank issue," said Candace Wiest, president and CEO at West Valley National Bank in Avondale. "But in reality, (the proposal) fixed fees for us, too."

The Independent Community Bankers of America and Arizona Bankers Association, both of which mainly represent small institutions, also oppose interchange caps. The ICBA said 93 percent of its members plan to charge for services currently offered for free if the swipe-fee cap is implemented.

Smaller banks don't have the diversified revenue sources of large banks, or their economies of scale, and thus would be at a competitive disadvantage.

Wiest calls the fee cap another worry for small banks, which already are facing rising regulatory costs from the Dodd-Frank reform legislation.

Twelve Arizona banks have failed since mid-2009, and two-thirds of the survivors lost money last year.

"A number of banks still have hurt coming at them if the economy doesn't improve substantially," Wiest said, adding that bankers will be forced to "find other ways to pass along the costs to consumers" if the fee cap takes effect.

The debate really boils down to switching revenue, or shifting costs, from one industry to the other. If the swipe-fee cap takes effect, it's anyone's guess how much of the savings would be passed along by retailers to consumers. How would anyone even measure this?

But there's no free lunch. Consumers will be affected, and likely pay, one way or another.

by Russ Wiles The Arizona Republic Feb. 27, 2011 12:00 AM

Sectors spar over fee cap on debit use

The fighting between the retail and financial industrials is over interchange fees on debit transactions. After years of merchant complaints, Congress in December instructed the Federal Reserve to cut the fees to 12 cents per swipe, down from an estimate of 44 cents or higher, depending on whom you talk to. Regardless, the change adds up to billions of dollars.

Merchants have been griping that these fees cut into their already-thin profit margins and prevent them from passing along lower prices to consumers.

Banks, credit unions and card issuers say the fees pay to implement and operate their debit systems and help absorb fraud costs.

Consumers don't foot the costs directly, although some merchants add surcharges, and many others are vocal about the costs they absorb. But consumers will be affected by how this debate plays out.

The Fed's fee cap is set to be adopted by April 21 and take effect three months later. The financial industry, with sympathy from some members of Congress, is seeking a delay.

Retailer groups call the current system anti-competitive. They say it allows Visa and MasterCard to fix swipe fees with no opportunity for bargaining or competition. They say swipe fees have tripled over the past decade even as bank costs have decreased.

"Rates have gone up unchecked for the last 10 years," said Tim McCabe, president of the Arizona Food Marketing Alliance, which represents 1,400 supermarkets, convenience stores and other retailers.

"As technology has advanced and we have gotten away from paper, you'd expect these fees to decrease, but they haven't."

The Merchants Payments Coalition, a national group of which the Arizona Food Marketing Alliance is a member, estimates the cap will generate $13 billion in annual savings for merchants and consumers.

Retailers have accused big banks of "scare tactics" to rally small banks and credit unions to their side.

The proposal does provide a fee-cap exemption for smaller banks and credit unions - those with assets below $10 billion. But it doesn't require that debit-payment networks distinguish between the two.

The Fed has solicited comments for the past two months, and Congress has held hearings, so it's possible the new rules could be altered or delayed.

"Quite frankly, some small issuers are concerned networks may not provide a two-tiered structure once the rule is final or may not maintain it into the future," said Mary Mitchell Dunn, a senior vice president at the Credit Union National Association, in a recent letter to the Fed.

"Without a two-tiered structure, there is no exemption."

CUNA and the 70 percent of credit unions that offer debit are "extremely concerned about the impact of this proposal on their members, their debit-card programs and their operations generally," she wrote.

Credit unions can't pass the buck to shareholders - because they don't have any. Instead, their members would feel the pain through increased fees for various services or lower interest rates paid on deposits.

CUNA estimates credit-union debit customers could face an average new annual fee of $34, a transaction fee of 25 cents per swipe or some combination.

Paul Stull, a vice president at Arizona State Credit Union, estimates the proposed fee cap would cost his institution more than $5 million annually.

"In the end, our members would pay higher fees or will have reduced services," he said.

Swipe fees also help banks and credit unions absorb fraud losses, including those caused by a merchant's failure to check identifications or otherwise validate purchases.

Stull cited a recent case in which crooks installed card-reading skimmers at Tucson-area gas stations and used the cardholder information they obtained to make fake ATM cards, employing those to extract illicit withdrawals.

"Our losses from that came to more than $10,000 within a few days," he said. "But the gas stations got all their money, and our members didn't lose any money."

Small community banks, which have been hit much harder than their large counterparts by the soft economy, also are worried.

"A lot of people look at it as a big-bank issue," said Candace Wiest, president and CEO at West Valley National Bank in Avondale. "But in reality, (the proposal) fixed fees for us, too."

The Independent Community Bankers of America and Arizona Bankers Association, both of which mainly represent small institutions, also oppose interchange caps. The ICBA said 93 percent of its members plan to charge for services currently offered for free if the swipe-fee cap is implemented.

Smaller banks don't have the diversified revenue sources of large banks, or their economies of scale, and thus would be at a competitive disadvantage.

Wiest calls the fee cap another worry for small banks, which already are facing rising regulatory costs from the Dodd-Frank reform legislation.

Twelve Arizona banks have failed since mid-2009, and two-thirds of the survivors lost money last year.

"A number of banks still have hurt coming at them if the economy doesn't improve substantially," Wiest said, adding that bankers will be forced to "find other ways to pass along the costs to consumers" if the fee cap takes effect.

The debate really boils down to switching revenue, or shifting costs, from one industry to the other. If the swipe-fee cap takes effect, it's anyone's guess how much of the savings would be passed along by retailers to consumers. How would anyone even measure this?

But there's no free lunch. Consumers will be affected, and likely pay, one way or another.

by Russ Wiles The Arizona Republic Feb. 27, 2011 12:00 AM

Sectors spar over fee cap on debit use

Saturday, February 26, 2011

Gilbert land buy facing scrutiny

Arizona Attorney General Tom Horne on Friday said that his office will likely examine a Gilbert land deal worth $50.2 million in search of any criminal wrongdoing.

For months, Gilbert officials have faced pressure and criticism from land experts and residents who say the town vastly overpaid for the property.

The Gilbert Town Council on Thursday called on the Attorney General's Office to investigate the transaction, but Horne said he'll wait for a formal request before pursuing the case. Once contacted, Horne said he'll assign an investigator to search for evidence of a crime.

"I think there would have to be some kind of improper motive," Horne said. "Just mere negligence is not a crime; it's a reason to not elect someone again."

Gilbert purchased the property in February 2009, acquiring 142.5 acres of undeveloped farmland, several right-of-way strips for road improvements, and dairy infrastructure from farmer Bernard Zinke.

Two large parcels are intended for future parks in an underserved area of south Gilbert, officials have said. Although officials expressed urgency in acquiring the land, there is no timetable for development, and funding for construction has not been allocated.

The Arizona Republic in September cited land experts who said the town's cost of $300,000 per acre was well over market value and came at a time when land values were sinking amid the recession.

The council's call for an outside investigation followed The Republic's disclosures this week that the town had a 2007 appraisal for a significant portion of the land that put its worth at $67,000 an acre, far less than the $300,000-per-acre price the council unanimously approved at the request of former Town Manager George Pettit.

No appraisal of the entire 142.5-acre site had been commissioned before the sale was approved, and the existence of the 2007 appraisal had never been disclosed by town officials.

Two of the primary negotiators on the Zinke land deal are no longer with the town: Pettit was forced into retirement last year, and former capital-projects coordinator Paul Mood took a job with Fountain Hills.

Senior program manager Jeff Kramer told The Republic that officials were aware of the existing appraisals - other appraisals were made in 2008 - while conducting negotiations but that other factors drove the deal.

During cost negotiations, "Zinke told me and Paul Mood what he wanted," Kramer said. "We then took that to the former town manager (Pettit)."

The council on Thursday directed current Town Manager Collin DeWitt to find an independent firm to conduct a forensic audit, which would attempt to "follow the money."

"Let them find out once and for all if there is any wrongdoing or if it was just bad business practice, poor negotiations or whatever it is," Councilman John Sentz said.

Councilwoman Jenn Daniels asked that any town documents related to the Zinke deal be made available to the public on the town's website.

"Sunlight is the best disinfectant," Daniels said. "I really don't feel satisfied at this time, and I don't think the public does, either."

by Parker Leavitt The Arizona Republic Feb. 26, 2011 12:00 AM

Gilbert land buy facing scrutiny

For months, Gilbert officials have faced pressure and criticism from land experts and residents who say the town vastly overpaid for the property.

The Gilbert Town Council on Thursday called on the Attorney General's Office to investigate the transaction, but Horne said he'll wait for a formal request before pursuing the case. Once contacted, Horne said he'll assign an investigator to search for evidence of a crime.

"I think there would have to be some kind of improper motive," Horne said. "Just mere negligence is not a crime; it's a reason to not elect someone again."

Gilbert purchased the property in February 2009, acquiring 142.5 acres of undeveloped farmland, several right-of-way strips for road improvements, and dairy infrastructure from farmer Bernard Zinke.

Two large parcels are intended for future parks in an underserved area of south Gilbert, officials have said. Although officials expressed urgency in acquiring the land, there is no timetable for development, and funding for construction has not been allocated.

The Arizona Republic in September cited land experts who said the town's cost of $300,000 per acre was well over market value and came at a time when land values were sinking amid the recession.

The council's call for an outside investigation followed The Republic's disclosures this week that the town had a 2007 appraisal for a significant portion of the land that put its worth at $67,000 an acre, far less than the $300,000-per-acre price the council unanimously approved at the request of former Town Manager George Pettit.

No appraisal of the entire 142.5-acre site had been commissioned before the sale was approved, and the existence of the 2007 appraisal had never been disclosed by town officials.

Two of the primary negotiators on the Zinke land deal are no longer with the town: Pettit was forced into retirement last year, and former capital-projects coordinator Paul Mood took a job with Fountain Hills.

Senior program manager Jeff Kramer told The Republic that officials were aware of the existing appraisals - other appraisals were made in 2008 - while conducting negotiations but that other factors drove the deal.

During cost negotiations, "Zinke told me and Paul Mood what he wanted," Kramer said. "We then took that to the former town manager (Pettit)."

The council on Thursday directed current Town Manager Collin DeWitt to find an independent firm to conduct a forensic audit, which would attempt to "follow the money."

"Let them find out once and for all if there is any wrongdoing or if it was just bad business practice, poor negotiations or whatever it is," Councilman John Sentz said.

Councilwoman Jenn Daniels asked that any town documents related to the Zinke deal be made available to the public on the town's website.

"Sunlight is the best disinfectant," Daniels said. "I really don't feel satisfied at this time, and I don't think the public does, either."

by Parker Leavitt The Arizona Republic Feb. 26, 2011 12:00 AM

Gilbert land buy facing scrutiny

Fannie, Freddie post losses

WASHINGTON - Government-controlled mortgage buyer Fannie Mae has posted a narrower loss of $2.1 billion for the October-December quarter of last year, and asked for an additional $2.6 billion in federal aid.

The new request is slightly more than the $2.5 billion it sought in the July-September quarter. The mortgage buyer also reported a $21.7 billion loss for all of 2010.

The government rescued Fannie Mae and sibling company Freddie Mac in September 2008 to cover their losses on soured mortgage loans.

It estimates the bailouts will cost taxpayers as much as $259 billion.

Fannie Mae's October-December loss attributable to common stockholders works out to 37 cents a share. It takes into account $2.2 billion in dividend payments to the government. It compares with a loss of $16.3 billion, or $2.87 a share, in the fourth quarter of 2009.

Freddie Mac managed a narrower loss of $1.7 billion for the October-December quarter of last year. But it has asked for an additional $500 million in federal aid - up from the $100 million it sought in the previous quarter.

Freddie Mac also posted a $19.8 billion loss for all of 2010.

Freddie Mac's October-December loss attributable to common stockholders works out to 53 cents a share. It takes into account $1.6 billion in dividend payments to the government.

It compares with a loss of $7.8 billion, or $2.39 a share, in the fourth quarter of 2009.

Associated Press Feb. 25, 2011 12:00 AM

Fannie, Freddie post losses

The new request is slightly more than the $2.5 billion it sought in the July-September quarter. The mortgage buyer also reported a $21.7 billion loss for all of 2010.

The government rescued Fannie Mae and sibling company Freddie Mac in September 2008 to cover their losses on soured mortgage loans.

It estimates the bailouts will cost taxpayers as much as $259 billion.

Fannie Mae's October-December loss attributable to common stockholders works out to 37 cents a share. It takes into account $2.2 billion in dividend payments to the government. It compares with a loss of $16.3 billion, or $2.87 a share, in the fourth quarter of 2009.

Freddie Mac managed a narrower loss of $1.7 billion for the October-December quarter of last year. But it has asked for an additional $500 million in federal aid - up from the $100 million it sought in the previous quarter.

Freddie Mac also posted a $19.8 billion loss for all of 2010.

Freddie Mac's October-December loss attributable to common stockholders works out to 53 cents a share. It takes into account $1.6 billion in dividend payments to the government.

It compares with a loss of $7.8 billion, or $2.39 a share, in the fourth quarter of 2009.

Associated Press Feb. 25, 2011 12:00 AM

Fannie, Freddie post losses

Sluggish new-home sales a drag on nation's growth

WASHINGTON - Sales of new homes plummeted in January, and businesses ordered fewer long-lasting goods. But the number of people applying for unemployment benefits has fallen over the past four weeks to the lowest level in 2 ½ years.

Together, the government reports Thursday sketched a mixed picture. They suggest that the struggling housing industry remains a drag on an economy that is growing slowly but steadily.

The reports showed:

• New-home sales dropped 12.6 percent last month to a seasonally adjusted annual rate of 284,000, the Commerce Department said. That's less than half of the pace economists consider healthy. The drop is a worrisome sign because it follows the worst year for new-home sales in nearly 50 years.

• Companies' orders for long-lasting manufactured goods, excluding the volatile aircraft and auto categories, dropped 3.6 percent last month, Commerce said in a separate report. The drop followed two months of gains. One category that is viewed as a proxy for business-investment spending fell by the largest amount in two years.

Overall, orders for durable goods rose 2.7 percent, driven by a jump in commercial-aircraft orders. Still, orders totaled about $200 billion. That's considered a healthy level, and it's 25 percent above the recession low hit in March 2009.

• Applications for unemployment benefits dropped by 22,000 last week to a seasonally adjusted 391,000, the Labor Department said. It was the third decline in four weeks.

The four-week average for applications, a less volatile figure, fell to 402,000. It was the fewest since late July 2008 and a sign that the job market is slowly improving.

Layoffs have fallen to pre-recession lows. And the downward trend in applications for unemployment benefits indicates they are dropping further. Still, employers aren't hiring enough to lower high unemployment.

Applications for unemployment benefits below 425,000 tend to signal modest job creation. But they would need to dip consistently to 375,000 or below to indicate a significant drop in the unemployment rate. Applications for benefits peaked during the recession at 651,000.

"While layoffs have come way down, new hiring hasn't picked up appreciably," said Cary Leahey, an economist at Decision Economics. "Many firms are still sitting on the fence."

That reluctance could continue for a few months, Leahey cautioned, because of the turmoil in the Middle East. That's pushing up oil and gas prices, which could leave consumers with less money to spend. Businesses may hold off on hiring for a few more months until the uncertainty clears.

The economy is growing. But the growth isn't happening fast enough to encourage aggressive hiring.

The nation's gross domestic product, the broadest gauge of the output of goods and services, rose at a 3.2 percent annual rate in the October-December quarter. The government will update its fourth-quarter estimate today. Economists think the figure will be revised up slightly to 3.3 percent.

One of the clouds hanging over the economy is the depressed housing market, which many analysts say hasn't yet bottomed out. Last year marked the fifth straight annual decline for new-home sales after they hit record highs during the housing boom.

Buyers purchased 322,000 new homes last year. It was the lowest annual total on record going back 47 years. Economists say it could take years before sales return to a healthy pace.

by Derek Kravitz and Christopher S. Rugaber Associated Press Feb. 25, 2011 12:00 AM

Sluggish new-home sales a drag on nation's growth

Together, the government reports Thursday sketched a mixed picture. They suggest that the struggling housing industry remains a drag on an economy that is growing slowly but steadily.

The reports showed:

• New-home sales dropped 12.6 percent last month to a seasonally adjusted annual rate of 284,000, the Commerce Department said. That's less than half of the pace economists consider healthy. The drop is a worrisome sign because it follows the worst year for new-home sales in nearly 50 years.

• Companies' orders for long-lasting manufactured goods, excluding the volatile aircraft and auto categories, dropped 3.6 percent last month, Commerce said in a separate report. The drop followed two months of gains. One category that is viewed as a proxy for business-investment spending fell by the largest amount in two years.

Overall, orders for durable goods rose 2.7 percent, driven by a jump in commercial-aircraft orders. Still, orders totaled about $200 billion. That's considered a healthy level, and it's 25 percent above the recession low hit in March 2009.

• Applications for unemployment benefits dropped by 22,000 last week to a seasonally adjusted 391,000, the Labor Department said. It was the third decline in four weeks.

The four-week average for applications, a less volatile figure, fell to 402,000. It was the fewest since late July 2008 and a sign that the job market is slowly improving.

Layoffs have fallen to pre-recession lows. And the downward trend in applications for unemployment benefits indicates they are dropping further. Still, employers aren't hiring enough to lower high unemployment.

Applications for unemployment benefits below 425,000 tend to signal modest job creation. But they would need to dip consistently to 375,000 or below to indicate a significant drop in the unemployment rate. Applications for benefits peaked during the recession at 651,000.

"While layoffs have come way down, new hiring hasn't picked up appreciably," said Cary Leahey, an economist at Decision Economics. "Many firms are still sitting on the fence."

That reluctance could continue for a few months, Leahey cautioned, because of the turmoil in the Middle East. That's pushing up oil and gas prices, which could leave consumers with less money to spend. Businesses may hold off on hiring for a few more months until the uncertainty clears.

The economy is growing. But the growth isn't happening fast enough to encourage aggressive hiring.

The nation's gross domestic product, the broadest gauge of the output of goods and services, rose at a 3.2 percent annual rate in the October-December quarter. The government will update its fourth-quarter estimate today. Economists think the figure will be revised up slightly to 3.3 percent.

One of the clouds hanging over the economy is the depressed housing market, which many analysts say hasn't yet bottomed out. Last year marked the fifth straight annual decline for new-home sales after they hit record highs during the housing boom.

Buyers purchased 322,000 new homes last year. It was the lowest annual total on record going back 47 years. Economists say it could take years before sales return to a healthy pace.

by Derek Kravitz and Christopher S. Rugaber Associated Press Feb. 25, 2011 12:00 AM

Sluggish new-home sales a drag on nation's growth

Arizona's banking industry improves

With just four statewide failures last year, Arizona's banking industry is on the road to recovery, a new report indicates.

Arizona-based banks lost a cumulative $68 million in 2010, but that was down from $416 million in red ink for 2009, the Federal Deposit Insurance Corp. said.

Also, the picture for non-current loans and non-performing assets brightened, and equity capital stabilized. Plus, Arizona's banks earned a higher spread between what they collect and pay in interest, and the percentage of unprofitable institutions decreased.

Banks across the nation had an even better year, achieving a three-year profit high of $87.5 billion, including $21.7 billion in the fourth quarter, helped by lower provisions for loan losses and improvements in loan quality.

That compared with a national banking profit of $12.5 billion in 2009.

"Overall, 2010 was a turnaround year, with four straight quarters of positive earnings," FDIC Chairman Sheila Bair said in a statement.

She cited rising industry profits and a growing percentage of banks participating in that trend.

Paul Hickman, president and chief executive officer of the Arizona Bankers Association, said the state's industry is improving in terms of loan losses, deposits and other measures.

"It's not looking like 2006, but things are getting better," Hickman said.

Four Arizona banks failed in 2010: Desert Hills, Towne Bank, First Arizona Savings and Copper Star.

That left Arizona with 40 locally based institutions, the FDIC said.

Arizona bank assets, largely consisting of loans, fell to $13.8 billion from $15 billion for the year, deposits dipped to $11.5 billion from $12.4 billion, and the employee count slipped to 3,654 from 3,980.

These numbers don't include the big national and regional players such as Wells Fargo, Chase and Bank of America, which dominate in terms of assets, deposits, employees and other measures but are based elsewhere.

One Arizona institution, Legacy Bank, has failed so far in 2011.

For 2010, the nation suffered 157 bank failures. But just 30 failed in the fourth quarter, prompting the FDIC to predict the worst is behind.

"We believe that the number of failures peaked in 2010, and we expect both the number and total assets of this year's failures to be lower," Bair said.

However, the number of banks on the FDIC's problem list continues to rise.

The agency doesn't identify those institutions.

Despite progress, Arizona's industry of smaller community banks is a shadow of its former self, prompting concerns about competition and local investment.

"The big banks, the ones everyone is going to, are sucking money out of the state," said Ernest Garfield of Interstate Bank Developers, a Scottsdale firm that helps small banks get started.

The effect, he said, is to remove deposits and other assets from Arizona that could be used for local investments and economic development.

Over the past two years, the number of Arizona-based banks has declined 30 percent, with jobs down 15 percent, loans and other assets down 15 percent, capital off 19 percent, and deposits down 8 percent.

by Russ Wiles The Arizona Republic Feb. 25, 2011 12:00 AM

Arizona's banking industry improves

Arizona-based banks lost a cumulative $68 million in 2010, but that was down from $416 million in red ink for 2009, the Federal Deposit Insurance Corp. said.

Also, the picture for non-current loans and non-performing assets brightened, and equity capital stabilized. Plus, Arizona's banks earned a higher spread between what they collect and pay in interest, and the percentage of unprofitable institutions decreased.

Banks across the nation had an even better year, achieving a three-year profit high of $87.5 billion, including $21.7 billion in the fourth quarter, helped by lower provisions for loan losses and improvements in loan quality.

That compared with a national banking profit of $12.5 billion in 2009.

"Overall, 2010 was a turnaround year, with four straight quarters of positive earnings," FDIC Chairman Sheila Bair said in a statement.

She cited rising industry profits and a growing percentage of banks participating in that trend.

Paul Hickman, president and chief executive officer of the Arizona Bankers Association, said the state's industry is improving in terms of loan losses, deposits and other measures.

"It's not looking like 2006, but things are getting better," Hickman said.

Four Arizona banks failed in 2010: Desert Hills, Towne Bank, First Arizona Savings and Copper Star.

That left Arizona with 40 locally based institutions, the FDIC said.

Arizona bank assets, largely consisting of loans, fell to $13.8 billion from $15 billion for the year, deposits dipped to $11.5 billion from $12.4 billion, and the employee count slipped to 3,654 from 3,980.

These numbers don't include the big national and regional players such as Wells Fargo, Chase and Bank of America, which dominate in terms of assets, deposits, employees and other measures but are based elsewhere.

One Arizona institution, Legacy Bank, has failed so far in 2011.

For 2010, the nation suffered 157 bank failures. But just 30 failed in the fourth quarter, prompting the FDIC to predict the worst is behind.

"We believe that the number of failures peaked in 2010, and we expect both the number and total assets of this year's failures to be lower," Bair said.

However, the number of banks on the FDIC's problem list continues to rise.

The agency doesn't identify those institutions.

Despite progress, Arizona's industry of smaller community banks is a shadow of its former self, prompting concerns about competition and local investment.

"The big banks, the ones everyone is going to, are sucking money out of the state," said Ernest Garfield of Interstate Bank Developers, a Scottsdale firm that helps small banks get started.

The effect, he said, is to remove deposits and other assets from Arizona that could be used for local investments and economic development.

Over the past two years, the number of Arizona-based banks has declined 30 percent, with jobs down 15 percent, loans and other assets down 15 percent, capital off 19 percent, and deposits down 8 percent.

by Russ Wiles The Arizona Republic Feb. 25, 2011 12:00 AM

Arizona's banking industry improves

Maricopa County home valuations fall 11%

Few Maricopa County homeowners will be surprised when they open their latest property valuations to learn that their homes are officially worth less than last year.

The county tax valuations that begin arriving in the mail today will show the fourth consecutive annual drop in home values for Valley property owners.

Residential-property values fell an average of 11 percent in 2010, according to the latest report from the Maricopa County Assessor's Office. But it also shows that the rate of annual decline in values is slowing.

In 2009, metro Phoenix residential property values fell 15 percent. In 2008, they plummeted 23 percent, the biggest drop of the prolonged retreat in home prices. In 2007, values declined 13 percent.

County Assessor Keith Russell said the valuations most homeowners receive in the mail in the next week will reflect the continued decline in property values.

The property-valuation assessments going out now will be reflected in 2012 tax bills.

Last year, the overall median value of homes in the county fell to $117,700 from $132,200 in 2009.

Some Valley cities fared better than others. Home values declined only 1.8 percent in Litchfield Park but plummeted 45.3 percent in Tolleson.

County homeowners have yet to see declines in their property taxes similar to the size of drops in property valuations, and they likely won't again this year.

Many Valley municipalities and school districts are still facing budget gaps and will likely have to raise property-tax rates this fall, effectively wiping out any tax reduction that the lower valuations would suggest.

Property-tax bills, which lag valuations by 18 months in Arizona, are based on a complex formula that includes funding for municipalities and school districts. Most property-tax money is spent on education.

The annual tax bill that homeowners will receive this September will be based on 2009's valuation, not on the new figures released today. The lag is built into Arizona's property-tax process so homeowners can appeal their valuations if they believe the initial appraisal is too high or low.

Property owners can appeal their valuations with the Assessor's Office until April 26.

About 1.5 million properties were valued by the Maricopa County assessor during 2009.

The county tax valuations that begin arriving in the mail today will show the fourth consecutive annual drop in home values for Valley property owners.

Residential-property values fell an average of 11 percent in 2010, according to the latest report from the Maricopa County Assessor's Office. But it also shows that the rate of annual decline in values is slowing.

In 2009, metro Phoenix residential property values fell 15 percent. In 2008, they plummeted 23 percent, the biggest drop of the prolonged retreat in home prices. In 2007, values declined 13 percent.

County Assessor Keith Russell said the valuations most homeowners receive in the mail in the next week will reflect the continued decline in property values.

The property-valuation assessments going out now will be reflected in 2012 tax bills.

Last year, the overall median value of homes in the county fell to $117,700 from $132,200 in 2009.

Some Valley cities fared better than others. Home values declined only 1.8 percent in Litchfield Park but plummeted 45.3 percent in Tolleson.

County homeowners have yet to see declines in their property taxes similar to the size of drops in property valuations, and they likely won't again this year.

Many Valley municipalities and school districts are still facing budget gaps and will likely have to raise property-tax rates this fall, effectively wiping out any tax reduction that the lower valuations would suggest.

Property-tax bills, which lag valuations by 18 months in Arizona, are based on a complex formula that includes funding for municipalities and school districts. Most property-tax money is spent on education.

The annual tax bill that homeowners will receive this September will be based on 2009's valuation, not on the new figures released today. The lag is built into Arizona's property-tax process so homeowners can appeal their valuations if they believe the initial appraisal is too high or low.

Property owners can appeal their valuations with the Assessor's Office until April 26.

About 1.5 million properties were valued by the Maricopa County assessor during 2009.

MORE ON THIS TOPIC

Maricopa County home valuations fall 11%

Understanding property taxes

Property-tax calculations and the terms used to discuss them can be confusing. Here are some basics:

- Full-cash value (FCV) is the figure that reflects a property's current market value. This number is used to calculate secondary taxes such as bonds, budget overrides and special districts such as fire and flood control.

- Limited property value (LPV) is used to assess taxes for school districts, cities, community colleges and the county. It's calculated using a complex formula set by the state Legislature and can't be higher than a property's FCV. The FCV and various LPVs from your assessment determine your share of taxes.

- Property taxes are determined through a formula based primarily on property valuations set by the county assessor and tax rates set by municipalities and school districts. Formulas vary from city to city. But here is an average breakdown of how much different kinds of taxing districts factor into property taxes: special districts, 7 percent; community college, 10 percent; county, 11 percent; cities, 11 percent; and schools, 61 percent. Financial decisions those groups make this summer will determine what property-tax bills look like this fall.

- The 18-month lag between property valuations and tax bills is built into the system so homeowners can appeal the values.

- The deadline to appeal a Maricopa County property valuation is April 26.

- For more information, go to www.maricopa.gov/assessor.

by Catherine Reagor The Arizona Republic Feb. 25, 2011 12:00 AMMaricopa County home valuations fall 11%

Investors snap up foreclosure bargains

WASHINGTON - Home sales are starting to tick up after the worst year in more than a decade. But the momentum is coming from cash-rich investors who are scooping up foreclosed properties at bargain prices, not first-time homebuyers who are critical for a housing recovery.

The number of first-time buyers fell last month to the lowest percentage in nearly two years, while all-cash deals have doubled and now account for one-third of sales.

A record number of foreclosures has forced home prices down in most markets. The median sales price for a home fell last month to its lowest level in nearly nine years, according to the National Association of Realtors.

Lower prices would normally be good for first-time homebuyers. But tighter lending standards have kept many from taking advantage of them. With fewer new buyers shopping, potential repeat buyers are hesitant to put their homes on the market and upgrade.

Cash-only investors are most interested in properties at risk of foreclosure. They can get those at bargain-basement prices.

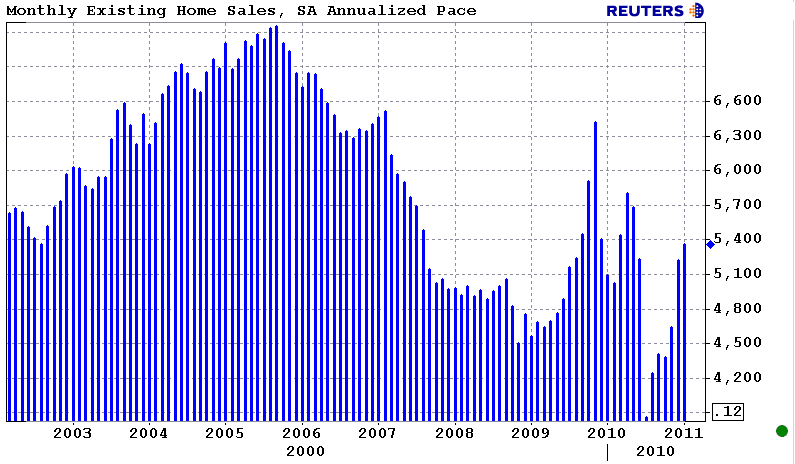

Sales of previously occupied homes rose slightly in January, to a seasonally adjusted annual rate of 5.36 million, the Realtors group said Wednesday. That's up 2.7 percent, from 5.22 million in December.

Still, the pace remains far below the 6 million homes a year that economists say represents a healthy market. And the number of first-time homebuyers fell to 29 percent of the market, the lowest percentage of the market in nearly two years. A more healthy level of first-time homebuyers is about 40 percent, according to the trade group.

Foreclosures represented 37 percent of sales in January. All-cash transactions accounted for 32 percent of home sales, twice the rate from two years ago, when the trade group began tracking these deals on a monthly basis. In places like Las Vegas and Miami, cash deals represent about half of sales.

In the three states where foreclosures are highest, at-risk homes make up at least two-thirds of all sales. In Florida, 63 percent of sales in January involved homes that were at risk of foreclosure, according to a Campbell/Inside Mortgage Finance survey. In Arizona and Nevada, a combined 72 percent of sales involved homes at risk of foreclosure.

A major barrier for first-time homebuyers is tighter lending standards adopted since the housing bubble burst. These have made mortgage loans tougher to acquire. Banks are also requiring buyers to put down a larger down payment. During the housing boom, buyers could purchase a home with little or no money down.

The median down payment rose to 22 percent last year in at least nine major U.S. cities, according to a survey by Zillow .com, a real-estate data firm. That's up from 4 percent in late 2006, as the housing bubble began to burst. The cities included some of the nation's hardest-hit markets - Las Vegas, Phoenix and Tampa - as well as areas that are rebounding, including San Diego and San Francisco.

by Derek Kravitz Associated Press Feb. 24, 2011 12:00 AM

Investors snap up foreclosure bargains

The number of first-time buyers fell last month to the lowest percentage in nearly two years, while all-cash deals have doubled and now account for one-third of sales.

A record number of foreclosures has forced home prices down in most markets. The median sales price for a home fell last month to its lowest level in nearly nine years, according to the National Association of Realtors.

Lower prices would normally be good for first-time homebuyers. But tighter lending standards have kept many from taking advantage of them. With fewer new buyers shopping, potential repeat buyers are hesitant to put their homes on the market and upgrade.

Cash-only investors are most interested in properties at risk of foreclosure. They can get those at bargain-basement prices.

Sales of previously occupied homes rose slightly in January, to a seasonally adjusted annual rate of 5.36 million, the Realtors group said Wednesday. That's up 2.7 percent, from 5.22 million in December.

Still, the pace remains far below the 6 million homes a year that economists say represents a healthy market. And the number of first-time homebuyers fell to 29 percent of the market, the lowest percentage of the market in nearly two years. A more healthy level of first-time homebuyers is about 40 percent, according to the trade group.

Foreclosures represented 37 percent of sales in January. All-cash transactions accounted for 32 percent of home sales, twice the rate from two years ago, when the trade group began tracking these deals on a monthly basis. In places like Las Vegas and Miami, cash deals represent about half of sales.

In the three states where foreclosures are highest, at-risk homes make up at least two-thirds of all sales. In Florida, 63 percent of sales in January involved homes that were at risk of foreclosure, according to a Campbell/Inside Mortgage Finance survey. In Arizona and Nevada, a combined 72 percent of sales involved homes at risk of foreclosure.

A major barrier for first-time homebuyers is tighter lending standards adopted since the housing bubble burst. These have made mortgage loans tougher to acquire. Banks are also requiring buyers to put down a larger down payment. During the housing boom, buyers could purchase a home with little or no money down.

The median down payment rose to 22 percent last year in at least nine major U.S. cities, according to a survey by Zillow .com, a real-estate data firm. That's up from 4 percent in late 2006, as the housing bubble began to burst. The cities included some of the nation's hardest-hit markets - Las Vegas, Phoenix and Tampa - as well as areas that are rebounding, including San Diego and San Francisco.

by Derek Kravitz Associated Press Feb. 24, 2011 12:00 AM

Investors snap up foreclosure bargains

Number of troubled banks rising

WASHINGTON - The number of banks at risk of failing made up nearly 12 percent of all federally insured banks in the final three months of 2010, the highest level in 18 years.

The Federal Deposit Insurance Corp said Wednesday the number of banks on its confidential "problem" list rose to 884 in the October-December quarter, up from 860 in the previous quarter. Those are banks rated by examiners as having very low capital cushions against risk.

Twenty-two banks failed so far this year. And more banks are at risk, even as the FDIC reported the industry's highest earnings as a group since the financial crisis hit three years ago.

Only a small fraction of the 7,657 federally insured banks - about 1.4 percent with assets of more than $10 billion - are driving the bulk of the earnings growth. They are the largest banks, including Bank of America Corp., Citigroup Inc., JPMorgan Chase & Co. and Wells Fargo & Co.

Big banks accounted for about $20.6 billion of the industry earnings of $21.7 billion in the fourth quarter. The total earnings compared with a net loss of $1.8 billion in the same quarter of 2009. The agency said bank earnings were buoyed in the latest quarter by reduced charges for soured loans.

Most of the big banks have recovered with help from federal bailout money and record-low borrowing rates.

Last year, 157 U.S. banks failed, the most in one year since 1992, the height of the savings and loan crisis. They were mostly smaller or regional banks. The failures compare with 25 in 2008 and three in 2007. They cost the federal deposit insurance fund an estimated $21 billion in 2010.

Associated Press Feb. 24, 2011 12:00 AM

The Federal Deposit Insurance Corp said Wednesday the number of banks on its confidential "problem" list rose to 884 in the October-December quarter, up from 860 in the previous quarter. Those are banks rated by examiners as having very low capital cushions against risk.

Twenty-two banks failed so far this year. And more banks are at risk, even as the FDIC reported the industry's highest earnings as a group since the financial crisis hit three years ago.

Only a small fraction of the 7,657 federally insured banks - about 1.4 percent with assets of more than $10 billion - are driving the bulk of the earnings growth. They are the largest banks, including Bank of America Corp., Citigroup Inc., JPMorgan Chase & Co. and Wells Fargo & Co.

Big banks accounted for about $20.6 billion of the industry earnings of $21.7 billion in the fourth quarter. The total earnings compared with a net loss of $1.8 billion in the same quarter of 2009. The agency said bank earnings were buoyed in the latest quarter by reduced charges for soured loans.

Most of the big banks have recovered with help from federal bailout money and record-low borrowing rates.

Last year, 157 U.S. banks failed, the most in one year since 1992, the height of the savings and loan crisis. They were mostly smaller or regional banks. The failures compare with 25 in 2008 and three in 2007. They cost the federal deposit insurance fund an estimated $21 billion in 2010.

Associated Press Feb. 24, 2011 12:00 AM

Trustee-sale date set for resort

Chandler's historic Crowne Plaza San Marcos Golf Resort is headed for foreclosure March 31, but the real-estate agent hired to market the property said it could sell before then.

Operation of the 98-year-old icon was taken over by a court-appointed receiver in October after San Marcos Capital partners defaulted on a $23.9 million loan from Guaranty Bank and Trust Co.

It has been on the market less than a month, and more than 70 potential buyers have shown an interest, said Sam Winterbottom, senior vice president for Grubb & Ellis in Atlanta. He would not disclose a price.

"The San Marcos resort has a lot of amenities that are hard to replicate with its historic golf course and hotel. It is well-known in the hotel industry," he said.

Opened in 1913, the facility is on the National Register of Historic Places and entertained the likes of Clark Gable, Fred Astaire, Joan Crawford, Christian Dior and President Herbert Hoover. It was Chandler's first large building and featured the state's first grass golf course.

According to documents filed with the Maricopa County Recorder, the foreclosure, a trustee sale, will be in the Ryley Carlock & Applewhite law offices in downtown Phoenix.

Winterbottom said it is rare in today's market for a resort trustee sale to attract bidders willing to pay more than the loan amount. If there are no outside bidders, ownership will be transferred to the lender, and the San Marcos will remain on the market if it hasn't sold, he said.

Frank Heavlin, a member of the defaulting partnership, and his wife, Darlene, were retained by the receiver to continue running the facility. When the financial troubles and receivership became public in October, that hurt business, Darlene Heavlin said. She fears the foreclosure news will deal another blow to operations and prompt event cancellations.

"So many hotels in the Valley have been affected (by the economy). It's a very difficult time for Arizona and the tourism business," she said.

The San Marcos has remained open during recent transitions, retained employees and honored contracts.

"This resort is going to stay open; it's a vital part of downtown. There are 15 restaurants and shops within walking distance. But my employees will be terrified and think they're going to lose their jobs," Darlene said.

City officials have expressed concern about the San Marcos' financial problems coming on the eve of the city and state's centennial celebrations in 2012, shortly after a new City Hall opened within walking distance of the resort and more than $11 million of enhancements to Arizona Avenue through downtown were done.

The resort's financial struggles and the recession also put Chandler's longtime hopes for a convention center on hold. In 2009, after consultants pointed to the area around the San Marcos as one of the best for conventions, the city started negotiations to build a 100,000-square-foot conference center on the property.

Those talks stopped when the owners defaulted, and the city has since delayed all non-essential building projects for five years or more because of declining tax revenues.

It is almost certain the next owner will keep the property as a resort, said Kirby Payne, the court-appointed receiver whose office is in Rhode Island. Strict zoning and city pride in the resort's history would make conversion to other uses unlikely, he said.

"This property has a fabulous history," he said. "More people are interested in it than we expected, and we've already had some offers but aren't considering them until we finish marketing."

Courts appoint receivers to take over day-to-day operations of troubled properties until financial issues are resolved through foreclosure or sale.

Teri Killgore, Chandler's downtown-redevelopment manager, said several potential buyers have contacted her to inquire about the city's involvement in downtown redevelopment.

Former Mayor Jerry Brooks said he expects the next owner "will get a really good deal on a tremendous asset."

When he was mayor during the mid-1980s, Brooks helped a group of Canadian investors secure tax-free bond financing to remodel and reopen the resort in 1987 after it had been closed for eight years.

by Edythe Jensen The Arizona Republic Feb. 24, 2011 12:00 AM

Trustee-sale date set for resort

Operation of the 98-year-old icon was taken over by a court-appointed receiver in October after San Marcos Capital partners defaulted on a $23.9 million loan from Guaranty Bank and Trust Co.

It has been on the market less than a month, and more than 70 potential buyers have shown an interest, said Sam Winterbottom, senior vice president for Grubb & Ellis in Atlanta. He would not disclose a price.

"The San Marcos resort has a lot of amenities that are hard to replicate with its historic golf course and hotel. It is well-known in the hotel industry," he said.

Opened in 1913, the facility is on the National Register of Historic Places and entertained the likes of Clark Gable, Fred Astaire, Joan Crawford, Christian Dior and President Herbert Hoover. It was Chandler's first large building and featured the state's first grass golf course.

According to documents filed with the Maricopa County Recorder, the foreclosure, a trustee sale, will be in the Ryley Carlock & Applewhite law offices in downtown Phoenix.

Winterbottom said it is rare in today's market for a resort trustee sale to attract bidders willing to pay more than the loan amount. If there are no outside bidders, ownership will be transferred to the lender, and the San Marcos will remain on the market if it hasn't sold, he said.

Frank Heavlin, a member of the defaulting partnership, and his wife, Darlene, were retained by the receiver to continue running the facility. When the financial troubles and receivership became public in October, that hurt business, Darlene Heavlin said. She fears the foreclosure news will deal another blow to operations and prompt event cancellations.

"So many hotels in the Valley have been affected (by the economy). It's a very difficult time for Arizona and the tourism business," she said.

The San Marcos has remained open during recent transitions, retained employees and honored contracts.

"This resort is going to stay open; it's a vital part of downtown. There are 15 restaurants and shops within walking distance. But my employees will be terrified and think they're going to lose their jobs," Darlene said.

City officials have expressed concern about the San Marcos' financial problems coming on the eve of the city and state's centennial celebrations in 2012, shortly after a new City Hall opened within walking distance of the resort and more than $11 million of enhancements to Arizona Avenue through downtown were done.

The resort's financial struggles and the recession also put Chandler's longtime hopes for a convention center on hold. In 2009, after consultants pointed to the area around the San Marcos as one of the best for conventions, the city started negotiations to build a 100,000-square-foot conference center on the property.

Those talks stopped when the owners defaulted, and the city has since delayed all non-essential building projects for five years or more because of declining tax revenues.

It is almost certain the next owner will keep the property as a resort, said Kirby Payne, the court-appointed receiver whose office is in Rhode Island. Strict zoning and city pride in the resort's history would make conversion to other uses unlikely, he said.

"This property has a fabulous history," he said. "More people are interested in it than we expected, and we've already had some offers but aren't considering them until we finish marketing."

Courts appoint receivers to take over day-to-day operations of troubled properties until financial issues are resolved through foreclosure or sale.

Teri Killgore, Chandler's downtown-redevelopment manager, said several potential buyers have contacted her to inquire about the city's involvement in downtown redevelopment.

Former Mayor Jerry Brooks said he expects the next owner "will get a really good deal on a tremendous asset."

When he was mayor during the mid-1980s, Brooks helped a group of Canadian investors secure tax-free bond financing to remodel and reopen the resort in 1987 after it had been closed for eight years.

by Edythe Jensen The Arizona Republic Feb. 24, 2011 12:00 AM

Trustee-sale date set for resort

Cash Buyers and Qualified Investors Prop Home Sales

The National Association of Realtors today released Existing Home Sales data for January 2011

Existing Home Sales report on the number of completed real estate sales transactions on single-family homes, townhomes, condominiums and co-ops. The methodology in calculating existing-home sales statistics is really quite simple. Each month the National Association of Realtor® receives data on existing-home sales from local associations/boards and multiple listing services (MLS) nationwide. The monthly EHS economic indicator is based on a representative sample of 160 Boards/MLSs. NAR captures 30-40% of all existing-home sale transactions with its monthly survey.

HERE is the methodology for the data collection

Excerpts from the January Release...

The uptrend in existing-home sales continues, with January sales rising for the third consecutive month with a pace that is now above year-ago levels, according to the National Association of REALTORS®.

Existing-home sales, which are completed transactions that include single-family, townhomes, condominiums and co-ops, increased 2.7 percent to a seasonally adjusted annual rate of 5.36 million in January from a downwardly revised 5.22 million in December, and are 5.3 percent above the 5.09 million level in January 2010. This is the first time in seven months that sales activity was higher than a year earlier.

Single-family home sales rose 2.4 percent to a seasonally adjusted annual rate of 4.69 million in January from 4.58 million in December, and are 4.9 percent higher than the 4.47 million level in January 2010. Existing condominium and co-op sales increased 4.7 percent to a seasonally adjusted annual rate of 670,000 in January from 640,000 in December, and are 7.9 percent above the 621,000-unit pace one year ago.

Lawrence Yun, NAR chief economist, said the improvement is good but could be better. “The uptrend in home sales is consistent with improvements in the economy and jobs, which are helping boost consumer confidence,” Yun said. “The extremely favorable housing affordability conditions are a big factor, but buyers have been constrained by unnecessarily tight credit. As a result, there are abnormally high levels of all-cash purchases, along with rising investor activity.”

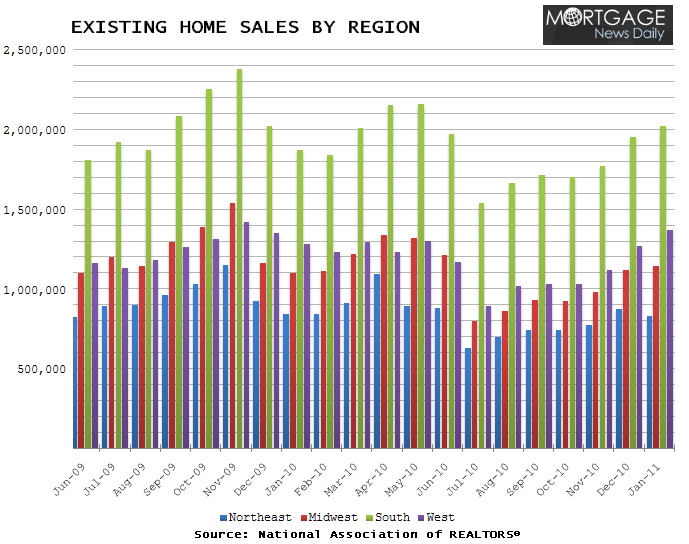

Regionally, existing-home sales in the Northeast fell 4.6 percent to an annual pace of 830,000 in January from a spike in December and are 1.2 percent below January 2010. Existing-home sales in the Midwest rose 1.8 percent in January to a level of 1.14 million and are 3.6 percent above a year ago. In the South, existing-home sales increased 3.6 percent to an annual pace of 2.02 million in January and are 8.0 percent higher than January 2010. Existing-home sales in the West rose 7.9 percent to an annual level of 1.37 million in January and are 7.0 percent above January 2010.

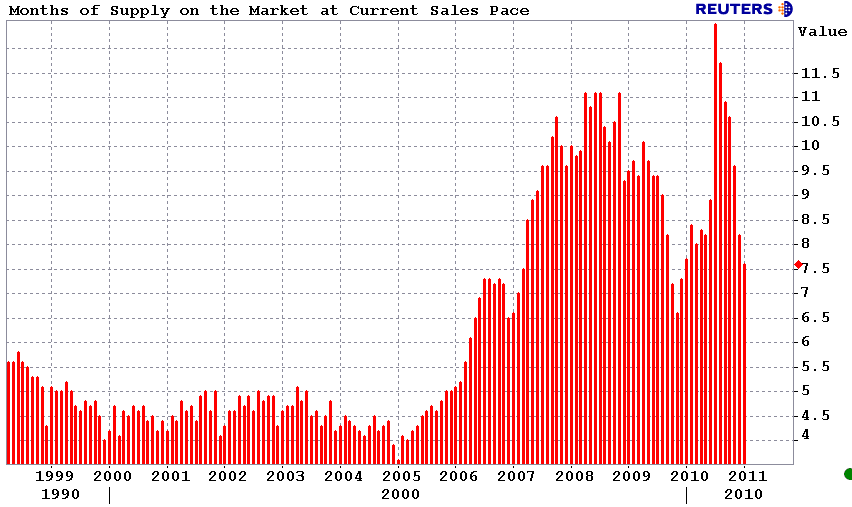

Total housing inventory at the end of January fell 5.1 percent to 3.38 million existing homes available for sale, which represents a 7.6-month supply at the current sales pace, down from an 8.2-month supply in December. The inventory supply is at the lowest level since December 2009 when there was a 7.3-month supply.

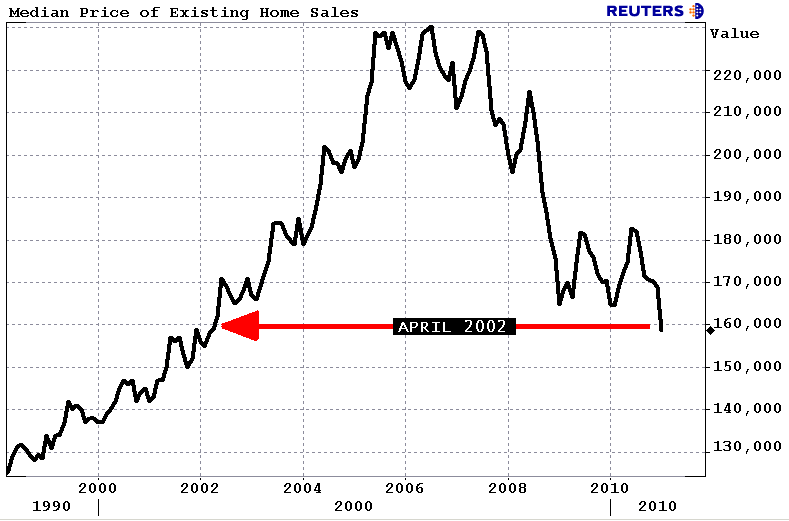

The national median existing-home price for all housing types was $158,800 in January, down 3.7 percent from January 2010. The median existing single-family home price was $159,400 in January, down 2.7 percent from a year ago. The median existing condo price was $154,900 in January, which is 10.2 percent below January 2010.

The median price in the Northeast was $236,500, which is 4.0 percent below a year ago. The median price in the Midwest was $126,300, which is 3.2 percent below January 2010. The median price in the South was $136,600, down 2.1 percent from a year ago. The median price in the West was $193,200, down 5.7 percent from a year ago.

NAR President Ron Phipps, broker-president of Phipps Realty in Warwick, R.I., said the median price is being dampened by unusual market factors. “Unprecedented levels of all-cash purchases, primarily of distressed homes sold at deep discounts, undoubtedly pulls the median price downward,” Phipps said. “Given the levels of inventory we see today, we believe that traditional homes in good condition have held their value.”

A parallel NAR practitioner survey shows first-time buyers purchased 29 percent of homes in January, down from 33 percent in December and 40 percent in January 2010 when an extended tax credit was in place. Investors accounted for 23 percent of purchases in January, up from 20 percent in December and 17 percent in January 2010; the balance of sales were to repeat buyers.

Distressed homes edged up to a 37 percent market share in January from 36 percent in December; it was 38 percent in January 2010.

All-cash sales rose to 32 percent in January from 29 percent in December and 26 percent in January 2010. All-cash purchases are at the highest level since NAR started measuring these purchases monthly in October 2008, when they accounted for 15 percent of the market. The average of all-cash deals was 20 percent in 2009, rising to 28 percent last year.

“Increases in all-cash transactions, the investor market share and distressed home sales all go hand-in-hand. With tight credit standards, it’s not surprising to see so much activity where cash is king and investors are taking advantage of conditions to purchase undervalued homes,” Yun said.

MND COMMENT: Even if it's cash buyers and investors, we gotta start somewhere! I live in D.C....this market is recovering well mostly thanks to BRAC and a stable job market. El Paso, Texas is another example of a city recovering faster than others because of military base realignments. There is value out there...just gotta find it.

by Adam Quinones Mortgage News Daily February 23, 2011

Fannie and Freddie: The Saga in Charts. - MarketBeat - WSJ

We admit it.

It’s hard for us to keep our eyelids propped open when Fannie and Freddie are brought up. We’re sure we’re not alone.

Yet the government controlled mortgage giants are once again in the news, with the Obama administration’s recently unveiled aproposal for winding them down. And given that this is MarketBeat, we figured we we should say something about these two crucial cogs in the not insignificant $10.6 trillion U.S. mortgage market.

So we figured we’d try to tell the story of Fannie and Freddie through some of the great charts The Journal has cobbled together in recent years on the two GSEs. The idea here is not that all the numbers will be completely up-to-date. (They can’t be. These charts are from older stories.) But we just want to try to make sense of the Fannie and Freddie mess for you.

But first things first. Exactly what do they do? The Journal’s Nick Timiraos, who covers Fannie and Freddie seems to have the best plainspoken explanation we’ve seen:

For 40 years, the housing-finance system has featured a blend of public and private entities. Fannie and Freddie buy mortgages from banks and other originators, repackage them for sale as securities and make investors whole when borrowers default. Investors long assumed the two shareholder-owned firms had an implied federal guarantee, which let them borrow at below-market rates and facilitate 30-year fixed-rate loans.

So what happened? Where to begin? Well we could go all the way back to the early 1930s when the U.S. first started getting involved in housing finance. (There’s a great timeline on page 10 of this report.)

But let’s just start during our recent housing mania. During the housing boom, Fannie and Freddie, which were publicly traded private companies — albeit with a fairly obvious backing of the Feds — began losing market share in the profitable business of buying up loans, packaging them up into securities and selling them off to investors.

The Journal reported that two companies, seeking to regain lost market share, loaded up on riskier subprime and Alt-A loans in 2006 and 2007 just as the housing market was starting to tank. As people began to have trouble paying their loans, some pretty ugly losses began to show up for Fannie and Freddie, like this.

Given the importance of Fannie and Freddie to the financial system — like other large banks such as Citigroup, et al. – the government didn’t let them collapse. As a result the bailout of Fannie and Freddie became a sizable part of the bailout mania of recent years. Check out this chart from April 2010.

Now, as this particularly ugly recession got underway the flow of cash from to borrowers — channeled through loans in the form of mortgage backed securities — dried up almost completely. Nobody wanted to go near the mortgage market given how ugly housing looked.

In fact, the only way investors appeared to willing to loan money for mortgages was if those bonds were backed by Fannie and Freddie, essentially the government. As a result, Fannie and Freddie — as well as Ginnie Mae, another government agency — now essentially backs the entire U.S. mortgage market. You can really see the private market disappearing in this chart.

And here’s a little fresher look, just at the government share.

Meanwhile, Fannie and Freddie have required huge injections of cash. Here’s a look from back in 2009:

Obviously this isn’t a sustainable situation. But with the economy looking pretty weak, at least until recently, there’s been plenty of reason for those in Washington to avoid rocking the boat. For instance, the government can use their mortgage buying ability to help keep mortgage rates down.

That may be helpful to the economy in the short term, but again no one thinks it’s sustainable in the long term. But here’s the problem, there just ain’t enough cash in the U.S. banking system to keep the mortgage market as big as it has been. That’s the reality.

But politicians know facing up to this reality would be expensive and painful for people. It’d get harder to borrow to buy a house. And it essentially it’d mean the American standard of living would go down. Not something anybody in Washington wants to see happen.

Hope that helps.

by Matt Phillips The Wall Street Journal February 11, 2011

Obama Administration Proposes Fannie Mae, Freddie Mac Phaseout - WSJ.com