Building-permit complaints in Phoenix increased by several hundred between 2010 and 2011, but far more cases were resolved before the city took them to court.

According to the Phoenix Planning and Development Department, the number of complaints rose to 1,446 from 1,135 between 2010 and 2011. The number of court cases dropped from 54 to six.

About half the increase in complaints can be attributed to a home appraiser who noted differences between homes he inspected and public records, said Mo Glancy, the department's deputy director.

Many of the rest are the result of "house flippers," investors who buy and remodel foreclosed homes without the necessary permits, he said.

About two-thirds of the violations were resolved in both years, simply by notifying the project owner who followed through with the required permits, Glancy said. Most of the others could not be verified, did not involve an active project or were the result of neighbor or family disputes, he said.

Glancy said responsibility for permit enforcement switched from the Neighborhood Services Department to the Planning and Development Department in August 2010, accounting for the drop in court cases.

"It is hard to get a resolution through the court," Glancy said. "We have tried to make resolution easy" by working with homeowners and contractors.

Phoenix issued about 20,000 building permits last year, about two-thirds of them for residential projects.

Most violations are the result of confusion about the requirements, which are in place to protect public health and safety, Glancy said. The city does not have enough personnel to check all projects but will follow up on complaints.

The cases that go to court are the most serious violations, Glancy said. In one case, a wedding facility went into operation without the needed permits, even though the owner had been alerted. That case is still in the works.

by Michael Clancy - Feb. 23, 2012 10:00 PM The Republic | azcentral.com

Building-permit complaints in Phoenix increased in 2011

Saturday, February 25, 2012

Report: Upbeat findings for Arizona housing market

Metro Phoenix home prices are up. Fewer inexpensive homes are for sale, and the number of pending foreclosures is down.

The positive housing-market update comes from Arizona State University's newest real-estate report.

It's the first monthly housing analysis from Mike Orr, who was recently named director of the Center for Real Estate Theory and Practice for ASU's W.P. Carey School of Business.

"Single-family home prices overall in the Phoenix area have been moving up since they reached a low point in September," Orr said in his debut monthly housing report.

"Also, looking forward, I expect a declining trend in foreclosures."

Orr also publishes a daily online analysis of Phoenix-area housing indicators called the "Cromford Report."

The median price of all home sales, including new homes, reached $120,500 in January of this year, Orr reports. That compares with $113,166 a year earlier.

The average price per square foot of Valley houses has climbed 3 percent since last year.

There were approximately 8,000 new and used homes sold in January, up from 7,500 in January 2011.

Orr said investors have snatched up the oversupply of homes for sale under $300,000.

"Many people think there's a glut of homes the banks are hiding somewhere, and that may be the case in other markets, but not here in the Phoenix area," he said.

"We've gone through so many foreclosures that the system has been working itself out for about five years."

In January, there were 2,450 single-family foreclosures in both Maricopa and Pinal counties, compared with 4,200 during January 2011, according to the ASU report.

The supply of homes listed for sale in metro Phoenix is down 42 percent from a year earlier.

by Catherine Reagor - Feb. 23, 2012 06:35 PM The Arizona Republic | azcentral.com

Report: Upbeat findings for Arizona housing market

Friday, February 24, 2012

Arizona bills target home-affidavit law

Leif Swanson expected an explosion of anger when homeowners received property-valuation notices this year.

But what he and many others feared turned out to be a dud.

The issue wasn't home values -- always a touchy subject -- but a requirement for an affidavit declaring the property is the owner's primary residence. Failure to return the affidavit could result in property taxes going up as much as $600 a year.

Swanson, a Realtor, said he was aware of the pending change and planned to notify his clients of it in his February newsletter. He, like others in the real-estate industry, worried homeowners would not scrutinize the annual statements and either toss them in a file or throw them away, risking a hit on their property taxes.

But when Swanson got his own valuation notice, there was no affidavit.

That's because the county assessors, who send out the valuation notices, didn't follow through on the affidavit, a provision of the Legislature's "jobs bill" that passed last year.

"The cost of doing it would have been considerable," Maricopa County Assessor Keith Russell said.

Besides, lawmakers had already signaled they intended to repeal the requirement because it was burdensome, Russell said, so it made little sense to whipsaw homeowners with a new requirement, only to walk it back. The result has been confusion in the real-estate ranks, said Tom Farley, CEO of the Arizona Association of Realtors. Those with long memories remember the debate at the Capitol in early 2011, when Farley warned that the affidavit could be easily overlooked and lead to unintended tax hikes.

That's because homeowners who actually live in their homes, as opposed to renting them out, automatically qualify for a rebate of up to $600 a year. Under last year's legislation, if a property owner didn't return the affidavit, he or she would lose the rebate.

"Our advice to homeowners right now is to sit tight," Farley said. "We're hoping this provision from last year's law will be repealed and a more targeted notice will be put in its place."

Lawmakers are speeding through two bills to do just that. One, Senate Bill 1217, has already passed the Senate and is awaiting a vote of the full House. The House version, House Bill 2486, which essentially does the same thing, is now in the Senate for action.

Rep. Debbie Lesko, R-Glendale, proposed the affidavit as a way to ferret out people who claim multiple properties as their primary residence and wrongly get a tax break.

It was rolled into the jobs bill to offset the money the state would lose from property-tax cuts for business and agriculture. Lawmakers figured the state would save $39 million a year by not granting the rebate to rental properties.

by Mary Jo Pitzl - Feb. 22, 2012 10:21 PM The Republic | azcentral.com

Arizona bills target home-affidavit law

But what he and many others feared turned out to be a dud.

The issue wasn't home values -- always a touchy subject -- but a requirement for an affidavit declaring the property is the owner's primary residence. Failure to return the affidavit could result in property taxes going up as much as $600 a year.

Swanson, a Realtor, said he was aware of the pending change and planned to notify his clients of it in his February newsletter. He, like others in the real-estate industry, worried homeowners would not scrutinize the annual statements and either toss them in a file or throw them away, risking a hit on their property taxes.

But when Swanson got his own valuation notice, there was no affidavit.

That's because the county assessors, who send out the valuation notices, didn't follow through on the affidavit, a provision of the Legislature's "jobs bill" that passed last year.

"The cost of doing it would have been considerable," Maricopa County Assessor Keith Russell said.

Besides, lawmakers had already signaled they intended to repeal the requirement because it was burdensome, Russell said, so it made little sense to whipsaw homeowners with a new requirement, only to walk it back. The result has been confusion in the real-estate ranks, said Tom Farley, CEO of the Arizona Association of Realtors. Those with long memories remember the debate at the Capitol in early 2011, when Farley warned that the affidavit could be easily overlooked and lead to unintended tax hikes.

That's because homeowners who actually live in their homes, as opposed to renting them out, automatically qualify for a rebate of up to $600 a year. Under last year's legislation, if a property owner didn't return the affidavit, he or she would lose the rebate.

"Our advice to homeowners right now is to sit tight," Farley said. "We're hoping this provision from last year's law will be repealed and a more targeted notice will be put in its place."

Lawmakers are speeding through two bills to do just that. One, Senate Bill 1217, has already passed the Senate and is awaiting a vote of the full House. The House version, House Bill 2486, which essentially does the same thing, is now in the Senate for action.

Rep. Debbie Lesko, R-Glendale, proposed the affidavit as a way to ferret out people who claim multiple properties as their primary residence and wrongly get a tax break.

It was rolled into the jobs bill to offset the money the state would lose from property-tax cuts for business and agriculture. Lawmakers figured the state would save $39 million a year by not granting the rebate to rental properties.

by Mary Jo Pitzl - Feb. 22, 2012 10:21 PM The Republic | azcentral.com

Arizona bills target home-affidavit law

Investors have eye on McDowell Corridor - USATODAY.com

Metro Phoenix residents are eager to see new life along the nearly 3-mile stretch of McDowell Road from Loop 101 to 64th Street.

It was standing-room only at a recent meeting of the Scottsdale City Council Subcommittee on Economic Development, where project representatives gave updates on their plans to kick-start revitalization on McDowell.

Residents learned that there already is new investment in the area and that more is on the way. In all, the corridor has attracted about $138million in private investment money in the past two years, said Jim Mullin, the city's economic-vitality director.

Those investments include apartment projects by Mark-Taylor and Chason Development, Chapman Ford's continued expansion, Fry's upcoming renovation, Comerica Bank, Chase Bank's expansion, Certified Benz & Beemer, and Paul's Ace Hardware renovation.

"There are two properties in escrow that, when announced, will bring the total to $150million, all since the city's Economic Development Department reorganization in November 2010," Mullin said.

That total doesn't include two major projects planned at SkySong, the Arizona State University Scottsdale Innovation Center.

And rising above it all could be an elevated trail in the center of McDowell that would go from the Indian Bend Wash just east of Miller Road to 64th Street at Papago Park and could include a 3,000- to 4,000-seat amphitheater at Papago Park. The proposal could be considered by voters in a bond proposal next year.

Current and future investments are aimed at bringing the McDowell Corridor "back to where it wants to be," Mullin said.

Mayor Jim Lane said there are no subsidies from the city in any of the projects involving that $138million investment.

New dealership

In 2008, Penske Automotive Group Inc. closed its Scottsdale Jaguar and Scottsdale Land Rover dealership at 6725 E. McDowell. Last November, Certified Benz & Beemer purchased the property from Penske and moved its pre-owned luxury-auto business from Mesa to McDowell.

"We started out in Mesa back in 2006, and we had 30 cars and 10 employees," manager Normand Neal said.

"Today, we have about 200 cars and over 40 employees, and we're estimating our annual sales this year to be about $45million."

A Scottsdale address better suits the business because of its focus on luxury autos, he said.

New residential

Chason Development, an upstate New York apartment developer, has purchased from Pitre Properties Ltd. a 5-acre site at the northwestern corner of McDowell and 68th Street. What was once an auto dealership will be transformed into a high-end apartment complex.

Zoning attorney John Berry said Chason plans to invest $25million in the project, which will include 220 units in one-, two- and three-story buildings, and reuse the existing parking garage.

The units along McDowell will feature stoops, or porches, with steps to bring the "activity out front."

"This is something we haven't seen in Scottsdale yet," Berry said.

The project would provide access to the nearby canal and could include landscaping the canal, he said.

In the meantime, Mark-Taylor expects to begin demolition next month to make way for its 536-unit luxury-apartment complex on 27 acres at the southeastern corner of 74th Street and McDowell.

The project represents a $75 million investment, and rents will average about $1,200 a month, said Scott Taylor, Mark-Taylor's president.

The project already has spurred commercial redevelopment in the area.

Fry's spokeswoman JoEllen Lynn said the Fry's store on McDowell west of Hayden Road will be remodeled and expanded in anticipation of the increased population in the area.

Work should begin in June with completion slated for January.

SkySong

Employment at SkySong has reached more than 1,000, and it has generated more than $397million in economic impact for the city since its inception, according to a new report from the Greater Phoenix Economic Council.

The complex, at the southeastern corner of Scottsdale Road and McDowell, now includes more than 70 companies and has reached 97 percent occupancy.

The foundation expects to have a third office building and a 325-unit apartment complex under construction at SkySong in the coming months.

Construction permits should be obtained within 90 days for the apartments, said Don Couvillion, vice president of real estate for the ASU Foundation.

Pre-leasing has begun for the third office building, SkySong III, he said.

By Edward Gately, The Republic|azcentral.com Feb 23, 2012

Investors have eye on McDowell Corridor - USATODAY.com

It was standing-room only at a recent meeting of the Scottsdale City Council Subcommittee on Economic Development, where project representatives gave updates on their plans to kick-start revitalization on McDowell.

Residents learned that there already is new investment in the area and that more is on the way. In all, the corridor has attracted about $138million in private investment money in the past two years, said Jim Mullin, the city's economic-vitality director.

Those investments include apartment projects by Mark-Taylor and Chason Development, Chapman Ford's continued expansion, Fry's upcoming renovation, Comerica Bank, Chase Bank's expansion, Certified Benz & Beemer, and Paul's Ace Hardware renovation.

"There are two properties in escrow that, when announced, will bring the total to $150million, all since the city's Economic Development Department reorganization in November 2010," Mullin said.

That total doesn't include two major projects planned at SkySong, the Arizona State University Scottsdale Innovation Center.

And rising above it all could be an elevated trail in the center of McDowell that would go from the Indian Bend Wash just east of Miller Road to 64th Street at Papago Park and could include a 3,000- to 4,000-seat amphitheater at Papago Park. The proposal could be considered by voters in a bond proposal next year.

Current and future investments are aimed at bringing the McDowell Corridor "back to where it wants to be," Mullin said.

Mayor Jim Lane said there are no subsidies from the city in any of the projects involving that $138million investment.

New dealership

In 2008, Penske Automotive Group Inc. closed its Scottsdale Jaguar and Scottsdale Land Rover dealership at 6725 E. McDowell. Last November, Certified Benz & Beemer purchased the property from Penske and moved its pre-owned luxury-auto business from Mesa to McDowell.

"We started out in Mesa back in 2006, and we had 30 cars and 10 employees," manager Normand Neal said.

"Today, we have about 200 cars and over 40 employees, and we're estimating our annual sales this year to be about $45million."

A Scottsdale address better suits the business because of its focus on luxury autos, he said.

New residential

Chason Development, an upstate New York apartment developer, has purchased from Pitre Properties Ltd. a 5-acre site at the northwestern corner of McDowell and 68th Street. What was once an auto dealership will be transformed into a high-end apartment complex.

Zoning attorney John Berry said Chason plans to invest $25million in the project, which will include 220 units in one-, two- and three-story buildings, and reuse the existing parking garage.

The units along McDowell will feature stoops, or porches, with steps to bring the "activity out front."

"This is something we haven't seen in Scottsdale yet," Berry said.

The project would provide access to the nearby canal and could include landscaping the canal, he said.

In the meantime, Mark-Taylor expects to begin demolition next month to make way for its 536-unit luxury-apartment complex on 27 acres at the southeastern corner of 74th Street and McDowell.

The project represents a $75 million investment, and rents will average about $1,200 a month, said Scott Taylor, Mark-Taylor's president.

The project already has spurred commercial redevelopment in the area.

Fry's spokeswoman JoEllen Lynn said the Fry's store on McDowell west of Hayden Road will be remodeled and expanded in anticipation of the increased population in the area.

Work should begin in June with completion slated for January.

SkySong

Employment at SkySong has reached more than 1,000, and it has generated more than $397million in economic impact for the city since its inception, according to a new report from the Greater Phoenix Economic Council.

The complex, at the southeastern corner of Scottsdale Road and McDowell, now includes more than 70 companies and has reached 97 percent occupancy.

The foundation expects to have a third office building and a 325-unit apartment complex under construction at SkySong in the coming months.

Construction permits should be obtained within 90 days for the apartments, said Don Couvillion, vice president of real estate for the ASU Foundation.

Pre-leasing has begun for the third office building, SkySong III, he said.

By Edward Gately, The Republic|azcentral.com Feb 23, 2012

Investors have eye on McDowell Corridor - USATODAY.com

Rising sales point to a stronger year for housing

WASHINGTON - The housing market is flashing signs of health ahead of the spring-buying season.

Sales of previously occupied homes are at their highest level since May 2010. More first-time buyers are making purchases. And the supply of homes fell last month to its lowest point in nearly seven years, which could push home prices higher.

Sales have now risen nearly 13 percent over the past six months. While they are still well below the 6 million that economists equate with a healthy market, the gains have coincided with other changes in the market that suggest more sales are coming.

"The trend is clearly upward," said Ian Shepherdson, chief U.S. economist at High Frequency Economics.

The National Association of Realtors said Wednesday that re-sales increased 4.3 percent last month to a seasonally adjusted annual rate of 4.57 million.

Single-family home sales rose 3.8 percent. And the number of first-time buyers, who are critical to a housing recovery, increased slightly to make up 33 percent of all sales. That's still below 40 percent, which tends to signal a healthy market.

One concern is that the market is still saturated with homes at risk of foreclosure, which lower broader home prices. Those increased to make up 35 percent of sales.

But the supply of homes on the market has plunged to 2.3 million, the lowest since March 2005. At last month's sales pace, it would take more than six months to clear those homes, consistent with a healthy housing market. Fewer homes on the market could help boost prices over time.

Most economists said the January report was encouraging, especially when viewed with other recent positive housing data.

Mortgage rates have never been lower. Homebuilders are slightly more hopeful because more people are saying they might be open to buying this year -- and they responded in January to that interest by requesting more permits to construct single-family homes.

"The rise in existing-home sales in recent months adds to the indication from housing starts, building permits and homebuilder sentiment that the sector has improved modestly since the middle of 2011," said John Ryding, an economist at RDQ economics.

Much of the optimism has come because hiring has picked up. More jobs are critical to a housing rebound. In January, employers added 243,000 net jobs -- the most in nine months -- and the unemployment rate fell to 8.3 percent, the lowest level in nearly three years.

Analysts caution that the damage from the housing bust is deep and the industry is years away from fully recovering. Since the bubble burst, sales have slumped under the weight of foreclosures, tighter credit and falling prices.

Many deals are also collapsing before they close. One-third of Realtors say they've seen at least one contract scuttled over the past four months. That's up from 18 percent in September.

Realtors say deals are collapsing for several reasons: Banks have declined mortgage applications. Home inspectors have found problems. Appraisals have come in lower than the bid. Or a buyer suffered a financial setback before the closing.

Sales rose across the country in January. They rose on a seasonal basis by nearly 9 percent in the West, 3.5 percent in the South, 3.4 percent in the Northeast and 1 percent in the Midwest.

by Derek Kravitz - Feb. 22, 2012 06:15 PM Associated Press

Rising sales point to a stronger year for housing

Sales of previously occupied homes are at their highest level since May 2010. More first-time buyers are making purchases. And the supply of homes fell last month to its lowest point in nearly seven years, which could push home prices higher.

Sales have now risen nearly 13 percent over the past six months. While they are still well below the 6 million that economists equate with a healthy market, the gains have coincided with other changes in the market that suggest more sales are coming.

"The trend is clearly upward," said Ian Shepherdson, chief U.S. economist at High Frequency Economics.

The National Association of Realtors said Wednesday that re-sales increased 4.3 percent last month to a seasonally adjusted annual rate of 4.57 million.

Single-family home sales rose 3.8 percent. And the number of first-time buyers, who are critical to a housing recovery, increased slightly to make up 33 percent of all sales. That's still below 40 percent, which tends to signal a healthy market.

One concern is that the market is still saturated with homes at risk of foreclosure, which lower broader home prices. Those increased to make up 35 percent of sales.

But the supply of homes on the market has plunged to 2.3 million, the lowest since March 2005. At last month's sales pace, it would take more than six months to clear those homes, consistent with a healthy housing market. Fewer homes on the market could help boost prices over time.

Most economists said the January report was encouraging, especially when viewed with other recent positive housing data.

Mortgage rates have never been lower. Homebuilders are slightly more hopeful because more people are saying they might be open to buying this year -- and they responded in January to that interest by requesting more permits to construct single-family homes.

"The rise in existing-home sales in recent months adds to the indication from housing starts, building permits and homebuilder sentiment that the sector has improved modestly since the middle of 2011," said John Ryding, an economist at RDQ economics.

Much of the optimism has come because hiring has picked up. More jobs are critical to a housing rebound. In January, employers added 243,000 net jobs -- the most in nine months -- and the unemployment rate fell to 8.3 percent, the lowest level in nearly three years.

Analysts caution that the damage from the housing bust is deep and the industry is years away from fully recovering. Since the bubble burst, sales have slumped under the weight of foreclosures, tighter credit and falling prices.

Many deals are also collapsing before they close. One-third of Realtors say they've seen at least one contract scuttled over the past four months. That's up from 18 percent in September.

Realtors say deals are collapsing for several reasons: Banks have declined mortgage applications. Home inspectors have found problems. Appraisals have come in lower than the bid. Or a buyer suffered a financial setback before the closing.

Sales rose across the country in January. They rose on a seasonal basis by nearly 9 percent in the West, 3.5 percent in the South, 3.4 percent in the Northeast and 1 percent in the Midwest.

by Derek Kravitz - Feb. 22, 2012 06:15 PM Associated Press

Rising sales point to a stronger year for housing

Expert: Building jobs on rebound

Construction employment is on the rise in Arizona and across the U.S., according to an economist who spoke Tuesday at a national construction-industry convention in Phoenix.

In 2011, Arizona construction jobs increased by 1.6 percent, the 11th-highest increase among the 50 states and the District of Columbia, according to Anirban Basu, chief economist for Arlington, Va.-based trade group Associated Builders and Contractors Inc.

The top-ranked state in 2011 for construction-job growth was North Dakota, where employment increased by 5.7 percent, due primarily to energy-related projects, Basu said.

Basu was among a group of economists, journalists and industry leaders who spoke at the 2012 BizCon convention, held Tuesday and Wednesday at the Arizona Biltmore hotel in Phoenix.

"The construction industry is now beginning to recover," he said.

Basu pointed to three key indicators of the construction industry's health, all of which have turned positive in recent months.

Construction employment had been on the rise in early 2011 but began to decrease in the summer, an aftershock from what Basu described as a "soft patch" in the nation's economic recovery, caused by high gas and food prices and a bitter fight in Congress over raising the debt ceiling.

The downward trend ended in November, and construction employment has since increased nationwide, he said.

"Construction is adding jobs in the country again," Basu said.

Another key indicator known as the Construction Backlog Index showed considerable recovery in 2011, he said, although it ended the year down slightly from its annual peak.

The index, which Associated Builders and Contractors releases quarterly, is an average of the backlog of work all U.S. construction companies have accrued, measured in months. An increase in the backlog is a sign of improvement.

In the fourth quarter, the reported index was 7.8 months, Basu said, down slightly from 8.1 months in both the second and third quarters but up 10.9 percent compared with the fourth quarter of 2010.

The third key indicator, known as the Architecture Billings Index, measures changes in the average amount of money architectural firms bill clients in a given month.

The American Institute of Architects, a Washington, D.C.-based trade group, reported slight architecture-billings increases in November and December following several months of decline.

Architecture billings are significant because they are a reliable leading indicator of future construction work, Basu said. He described the boost in economic indicators as a positive, early sign of recovery but said the industry still has a long way to go.

"We are on the mend," Basu said.

by J. Craig Anderson - Feb. 22, 2012 05:27 PM The Republic | azcentral.com

Expert: Building jobs on rebound

In 2011, Arizona construction jobs increased by 1.6 percent, the 11th-highest increase among the 50 states and the District of Columbia, according to Anirban Basu, chief economist for Arlington, Va.-based trade group Associated Builders and Contractors Inc.

The top-ranked state in 2011 for construction-job growth was North Dakota, where employment increased by 5.7 percent, due primarily to energy-related projects, Basu said.

Basu was among a group of economists, journalists and industry leaders who spoke at the 2012 BizCon convention, held Tuesday and Wednesday at the Arizona Biltmore hotel in Phoenix.

"The construction industry is now beginning to recover," he said.

Basu pointed to three key indicators of the construction industry's health, all of which have turned positive in recent months.

Construction employment had been on the rise in early 2011 but began to decrease in the summer, an aftershock from what Basu described as a "soft patch" in the nation's economic recovery, caused by high gas and food prices and a bitter fight in Congress over raising the debt ceiling.

The downward trend ended in November, and construction employment has since increased nationwide, he said.

"Construction is adding jobs in the country again," Basu said.

Another key indicator known as the Construction Backlog Index showed considerable recovery in 2011, he said, although it ended the year down slightly from its annual peak.

The index, which Associated Builders and Contractors releases quarterly, is an average of the backlog of work all U.S. construction companies have accrued, measured in months. An increase in the backlog is a sign of improvement.

In the fourth quarter, the reported index was 7.8 months, Basu said, down slightly from 8.1 months in both the second and third quarters but up 10.9 percent compared with the fourth quarter of 2010.

The third key indicator, known as the Architecture Billings Index, measures changes in the average amount of money architectural firms bill clients in a given month.

The American Institute of Architects, a Washington, D.C.-based trade group, reported slight architecture-billings increases in November and December following several months of decline.

Architecture billings are significant because they are a reliable leading indicator of future construction work, Basu said. He described the boost in economic indicators as a positive, early sign of recovery but said the industry still has a long way to go.

"We are on the mend," Basu said.

by J. Craig Anderson - Feb. 22, 2012 05:27 PM The Republic | azcentral.com

Expert: Building jobs on rebound

Paradise Valley residents get first glimpse of resort plan

Paradise Valley residents are getting their first glimpse of plans for the renovation of the shuttered Mountain Shadows resort.

Specifics are still minimal, but officials with JDM Partners LLC expect more information to be available when their special-use permit is submitted in the next week.

Stephen Earl, zoning counsel for the developer, said the firm's permit application is nearly complete. The Town Council met Friday to go over plans for the resort, at 56th Street and Lincoln Drive, on the northeastern side of Camelback Mountain. The resort closed in September 2004, but residences on the property are still in use.

JDM agreed to buy the 68-acre property late last year.

"We've been working intensely on this for the last month and a half, but we're not quite ready to file the (special-use permit)," Earl said. "We have a draft and hope to file very soon, but we don't know yet."

JDM, co-owned by sports businessman Jerry Colangelo, has projects that include Chase Field, US Airways Center and Comerica Theatre.

The company's purchase of the Wigwam resort in Litchfield Park about two years ago marked its first foray into the hospitality industry. The parties involved with the resort in Paradise Valley are looking to JDM's experience in the renovation of the 82-year-old Wigwam as a touchstone for Mountain Shadows.

Architect Erik Peterson, principal with PHX Architecture, said the team that worked on the Wigwam is working on the Mountain Shadows project.

Litchfield Park officials have said that sustainable changes were made to the Wigwam's pool areas, restaurants and bars, and that events like golf tournaments are beginning to draw more visitors to the Southwest Valley city.

"The Wigwam was rundown, broken and in disrepair," Peterson said.

The Mountain Shadows resort plan for renovation includes residential and retail components.

Peterson said the site will be reminiscent of California resort destinations like those in Santa Barbara.

Paradise Valley Town Councilman Michael Collins said past plans formally submitted for the Mountain Shadows site never truly captured the opportunity for the historic resort to be a legacy project -- something that transcends rudimentary development calculations, with the owners making a long-lasting contribution to the fabric and quality of life of the community.

Collins served on the Planning Commission for three years before being elected to the council in 2010.

He said the current concept embraces the proposed 2012 General Plan update, with a low-density resort town center that provides amenities to Mountain Shadows residents and includes a limited amount of community-oriented commercial services.

The General Plan update goes before voters on March 13.

"None of the plans before spoke to the true heritage of the site as a community gathering place," he said.

by Philip Haldiman - Feb. 23, 2012 10:30 AM The Republic | azcentral.com

Paradise Valley residents get first glimpse of resort plan

Specifics are still minimal, but officials with JDM Partners LLC expect more information to be available when their special-use permit is submitted in the next week.

Stephen Earl, zoning counsel for the developer, said the firm's permit application is nearly complete. The Town Council met Friday to go over plans for the resort, at 56th Street and Lincoln Drive, on the northeastern side of Camelback Mountain. The resort closed in September 2004, but residences on the property are still in use.

JDM agreed to buy the 68-acre property late last year.

"We've been working intensely on this for the last month and a half, but we're not quite ready to file the (special-use permit)," Earl said. "We have a draft and hope to file very soon, but we don't know yet."

JDM, co-owned by sports businessman Jerry Colangelo, has projects that include Chase Field, US Airways Center and Comerica Theatre.

The company's purchase of the Wigwam resort in Litchfield Park about two years ago marked its first foray into the hospitality industry. The parties involved with the resort in Paradise Valley are looking to JDM's experience in the renovation of the 82-year-old Wigwam as a touchstone for Mountain Shadows.

Architect Erik Peterson, principal with PHX Architecture, said the team that worked on the Wigwam is working on the Mountain Shadows project.

Litchfield Park officials have said that sustainable changes were made to the Wigwam's pool areas, restaurants and bars, and that events like golf tournaments are beginning to draw more visitors to the Southwest Valley city.

"The Wigwam was rundown, broken and in disrepair," Peterson said.

The Mountain Shadows resort plan for renovation includes residential and retail components.

Peterson said the site will be reminiscent of California resort destinations like those in Santa Barbara.

Paradise Valley Town Councilman Michael Collins said past plans formally submitted for the Mountain Shadows site never truly captured the opportunity for the historic resort to be a legacy project -- something that transcends rudimentary development calculations, with the owners making a long-lasting contribution to the fabric and quality of life of the community.

Collins served on the Planning Commission for three years before being elected to the council in 2010.

He said the current concept embraces the proposed 2012 General Plan update, with a low-density resort town center that provides amenities to Mountain Shadows residents and includes a limited amount of community-oriented commercial services.

The General Plan update goes before voters on March 13.

"None of the plans before spoke to the true heritage of the site as a community gathering place," he said.

by Philip Haldiman - Feb. 23, 2012 10:30 AM The Republic | azcentral.com

Paradise Valley residents get first glimpse of resort plan

Wednesday, February 15, 2012

Builder Sentiment Up Again « Eye on Housing

The NAHB/Wells Fargo Housing Market Index (HMI) increased four points in February to 29, the highest level since April 2007. The increase marks the fifth consecutive month of an increase for a total of 15 points since recording a 14 in September 2011. All three components also recorded levels not seen since early 2007. The current and future sales components both increased six points to 31 and 35 respectively. The traffic component rose two points to 23. Three of the four regional indexes rose while the South indicator fell two points to 26.

The steady increase in the HMI supports other consistent positive advances in housing indicators including an eight consecutive month rise in three-month moving average housing starts, a similar steady climb in single-family housing permits, and a five month rise in the NAHB/First American Improving Markets Index.

The HMI closely tracks single-family housing starts over its history and NAHB expects single-family starts to rise slowly in 2012 to 500,000, a 16% improvement over 2011. The improvements will be scattered and strongest in markets where the mid-2000s crash did the least damage to the underlying housing and employment markets.

by National Association of Home Builders Feb 15, 2012

by National Association of Home Builders Feb 15, 2012

Builder Sentiment Up Again « Eye on Housing

Monday, February 13, 2012

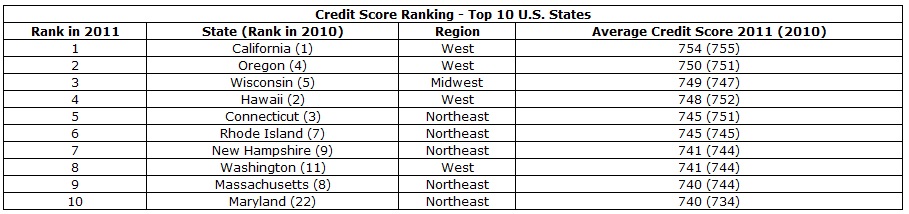

California Mortgage Applicants Tops in the Nation With Highest Credit Scores | Mortgage News | Daily National and State Headlines

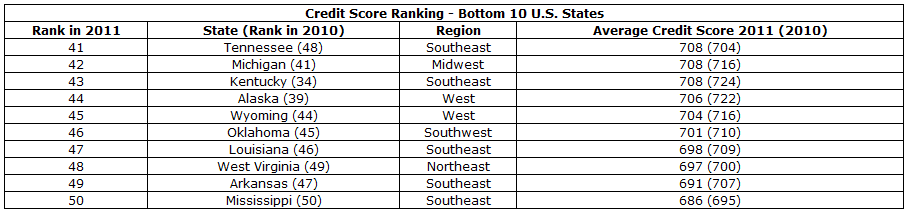

A study conducted by Mortgage Marvel has concluded that California mortgage applicants, for the second year in a row, have the highest average credit scores in the nation at 754—a full 24 points above the national average of 730. Mississippi mortgage applicants, again for the second year in a row, had the lowest average credit score of 686, 44 points below the national average. The information was compiled by analyzing more than 330,000 mortgage applications received in 2011 by clients of Mortgagebot, a D+H company. Mortgagebot is the owner of Mortgage Marvel and the provider of the PowerSite suite of integrated point-of-sale solutions.

Of the states with the highest average credit scores, four are in the West and five are in the Northeast. There was only one state in the top 10, Wisconsin, from another region (Midwest).

The Southeast occupied five of the 10 lowest credit score positions. Mississippi, for the second year in a row, had the nation's lowest average credit score.

by NationalMortgageProfessionals.com Feb 10, 2012

Arizona gets $1.6 billion in mortgage fraud settlement

Marking a watershed day in the aftermath of the national housing crash, Arizona officials announced a pair of settlements with large banks over allegations of improper lending and foreclosure practices that will result in more than a billion dollars of aid for struggling homeowners.

Arizona's portion of a nationwide, $26 billion settlement with the country's five biggest lenders will be $1.6 billion, the third-largest share after hard-hit California and Florida.

Most of the money in that deal, announced Thursday after negotiations by attorneys general across the country, will be paid out by lenders in the form of principal reductions -- cutting the amount of money that certain borrowers are responsible for repaying on their home loans. Lenders will also dedicate part of the funds to reducing other borrowers' interest payments and will issue $2,000 payments to people who lost homes in improperly managed foreclosures.

A second, smaller settlement with Bank of America ends a state lawsuit over the bank's lending practices and will fund consumer protection and future investigation of mortgage lending.

The national settlement will not deliver assistance to every struggling homeowner. It applies only to mortgages held by the five large lenders and does not extend to borrowers with loans backed by federal mortgage giants Fannie Mae and Freddie Mac, who make up more than half of all mortgage-holders.

Still, federal officials estimate that 60,000 Arizona borrowers could see assistance with their principal or interest rates. And the settlement marks the first time lenders have agreed, on any large scale, to forgive money owed by underwater borrowers.

"These settlements will help Arizona homeowners and the state's economy that is so tied to housing," Arizona Attorney General Tom Horne said. "I think we are holding banks accountable."

Who benefits

Only borrowers with loans owned by BofA, Citigroup, the former GMAC (now known as Ally Financial), JPMorgan Chase and Wells Fargo are eligible for aid from the national settlement. The five lenders are responsible for contacting eligible homeowners in the coming month to offer assistance.

The deal requires the banks to reduce loans for about 1 million households that are at risk of foreclosure. The lenders will also send $2,000 each to about 750,000 Americans who were improperly foreclosed upon from 2008 through 2011. The banks will have three years to fulfill terms of the deal.

Borrowers who had loans originally issued by the five participating lenders but then had their mortgages sold to another bank aren't eligible.

About $1.3 billion of Arizona's $1.6 billion will go toward principal reductions. Federal officials estimate the national average for principal reductions will be $20,000 per loan. In Arizona, where home prices have fallen 60 percent, many homeowners are likely to be underwater by far more than $20,000.

Horne said homeowners whose mortgage balances are 175 percent or more of their current home values and who are current on their payments will probably be the first to receive principal reductions.

Nationally, at least $17 billion of the settlement is to go directly to reducing principal. Details on how much lenders will reduce the amount borrowers owe aren't available yet.

About $86 million of Arizona's share of the deal will go toward offers to modify borrowers' loans by lowering interest rates. An additional $110.4 million has been set aside to compensate Arizona borrowers who lost their homes to foreclosure from 2008 to 2011 and believe they suffered unfair treatment by lender servicers. Each borrower is eligible for $2,000.

Horne said that any former homeowner who thinks he or she qualifies for the $2,000 should contact the lender and that little documentation will be required to receive this compensation.

Shaun Donovan, secretary of the U.S. Department of Housing and Urban Development, said 55,000 former Arizona homeowners will qualify for the $2,000 payments. During the housing crash, more than 175,000 borrowers have had Arizona homes taken back by lenders, though that figure includes loans held by Fannie and Freddie.

Arizona will receive $102.5 million to be used for mortgage-fraud investigations and consumer counseling.

Arizona State University's real-estate analyst Mike Orr said reducing mortgage principal for underwater homeowners will "significantly bolster the housing market" if it entices more people to stay in their homes and keep making payments.

Almost 50 percent of the state's homeowners are underwater, meaning homeowners owe more than their homes are now worth because values have plunged by more than half since the market's peak in 2006.

Patricia Garcia Duarte, president of the Phoenix-based housing non-profit Neighborhood Housing Services, said the settlement looks like a lot of money to help both former and current homeowners. However, she said the damage done to Arizona families and communities has been extreme.

"The funds will definitely help," Garcia Duarte said. "But how the funds are spent in Arizona will determine the success in our housing recovery."

BofA lawsuit

Arizona is also receiving $10 million through the settlement of a lawsuit with BofA over allegations of mortgage fraud and deceiving borrowers trying to obtain loan modifications.

The money will go toward funding criminal loan investigation and consumer education. Horne said it's not clear yet whether the BofA borrowers who served as plaintiffs will be compensated from the $10 million or the state's $1.6 billion from the national settlement.

The suit, filed in December 2010 by the state's attorney general, had to be reconciled for Arizona to participate in the national settlement.

"If we had continued to litigate the BofA lawsuit, we might have recovered more money," Horne said. "But the lawsuit could have taken another five to six years. By settling now and joining the national settlement, more homeowners will receive help sooner."

Enforcement

The deal establishes a regulatory group of local and federal government agencies. It calls for North Carolina's banking regulator Joseph Smith to monitor lenders for compliance.

Horne said lenders will be subject to hefty fines if they don't follow through with the actions to help homeowners laid out in the settlement.

Federal officials said states could receive more funding if more mortgage firms sign onto the agreement. One estimate is for the national settlement to grow to $40 billion if the next nine large lenders join in. The only state not part of the national settlement is Oklahoma. Arizona, California, Florida, New York and Nevada were the last states to join. Arizona's negotiations with BofA over the mortgage-fraud lawsuit went on until almost 11 p.m. Wednesday night.

President Barack Obama said in a speech Thursday that the $26 billion settlement will allow the nation's biggest banks, "banks rescued by taxpayer dollars," to right wrongs committed in making loans and foreclosing on homeowners during the past several years.

"These banks will put billions of dollars towards relief for families across the nation. They'll provide refinancing for borrowers that are stuck in high interest-rate mortgages," Obama said. "They'll reduce loans for families who owe more on their homes than they're worth. And they will deliver some measure of justice for families that have already been victims of abusive practices."

12 News reporter Melissa Blasius contributed to this article.

by Catherine Reagor - Feb. 9, 2012 09:28 AM The Republic | azcentral.com

Arizona gets $1.6 billion in mortgage fraud settlement

Arizona's portion of a nationwide, $26 billion settlement with the country's five biggest lenders will be $1.6 billion, the third-largest share after hard-hit California and Florida.

Most of the money in that deal, announced Thursday after negotiations by attorneys general across the country, will be paid out by lenders in the form of principal reductions -- cutting the amount of money that certain borrowers are responsible for repaying on their home loans. Lenders will also dedicate part of the funds to reducing other borrowers' interest payments and will issue $2,000 payments to people who lost homes in improperly managed foreclosures.

A second, smaller settlement with Bank of America ends a state lawsuit over the bank's lending practices and will fund consumer protection and future investigation of mortgage lending.

The national settlement will not deliver assistance to every struggling homeowner. It applies only to mortgages held by the five large lenders and does not extend to borrowers with loans backed by federal mortgage giants Fannie Mae and Freddie Mac, who make up more than half of all mortgage-holders.

Still, federal officials estimate that 60,000 Arizona borrowers could see assistance with their principal or interest rates. And the settlement marks the first time lenders have agreed, on any large scale, to forgive money owed by underwater borrowers.

"These settlements will help Arizona homeowners and the state's economy that is so tied to housing," Arizona Attorney General Tom Horne said. "I think we are holding banks accountable."

Who benefits

Only borrowers with loans owned by BofA, Citigroup, the former GMAC (now known as Ally Financial), JPMorgan Chase and Wells Fargo are eligible for aid from the national settlement. The five lenders are responsible for contacting eligible homeowners in the coming month to offer assistance.

The deal requires the banks to reduce loans for about 1 million households that are at risk of foreclosure. The lenders will also send $2,000 each to about 750,000 Americans who were improperly foreclosed upon from 2008 through 2011. The banks will have three years to fulfill terms of the deal.

Borrowers who had loans originally issued by the five participating lenders but then had their mortgages sold to another bank aren't eligible.

About $1.3 billion of Arizona's $1.6 billion will go toward principal reductions. Federal officials estimate the national average for principal reductions will be $20,000 per loan. In Arizona, where home prices have fallen 60 percent, many homeowners are likely to be underwater by far more than $20,000.

Horne said homeowners whose mortgage balances are 175 percent or more of their current home values and who are current on their payments will probably be the first to receive principal reductions.

Nationally, at least $17 billion of the settlement is to go directly to reducing principal. Details on how much lenders will reduce the amount borrowers owe aren't available yet.

About $86 million of Arizona's share of the deal will go toward offers to modify borrowers' loans by lowering interest rates. An additional $110.4 million has been set aside to compensate Arizona borrowers who lost their homes to foreclosure from 2008 to 2011 and believe they suffered unfair treatment by lender servicers. Each borrower is eligible for $2,000.

Horne said that any former homeowner who thinks he or she qualifies for the $2,000 should contact the lender and that little documentation will be required to receive this compensation.

Shaun Donovan, secretary of the U.S. Department of Housing and Urban Development, said 55,000 former Arizona homeowners will qualify for the $2,000 payments. During the housing crash, more than 175,000 borrowers have had Arizona homes taken back by lenders, though that figure includes loans held by Fannie and Freddie.

Arizona will receive $102.5 million to be used for mortgage-fraud investigations and consumer counseling.

Arizona State University's real-estate analyst Mike Orr said reducing mortgage principal for underwater homeowners will "significantly bolster the housing market" if it entices more people to stay in their homes and keep making payments.

Almost 50 percent of the state's homeowners are underwater, meaning homeowners owe more than their homes are now worth because values have plunged by more than half since the market's peak in 2006.

Patricia Garcia Duarte, president of the Phoenix-based housing non-profit Neighborhood Housing Services, said the settlement looks like a lot of money to help both former and current homeowners. However, she said the damage done to Arizona families and communities has been extreme.

"The funds will definitely help," Garcia Duarte said. "But how the funds are spent in Arizona will determine the success in our housing recovery."

BofA lawsuit

Arizona is also receiving $10 million through the settlement of a lawsuit with BofA over allegations of mortgage fraud and deceiving borrowers trying to obtain loan modifications.

The money will go toward funding criminal loan investigation and consumer education. Horne said it's not clear yet whether the BofA borrowers who served as plaintiffs will be compensated from the $10 million or the state's $1.6 billion from the national settlement.

The suit, filed in December 2010 by the state's attorney general, had to be reconciled for Arizona to participate in the national settlement.

"If we had continued to litigate the BofA lawsuit, we might have recovered more money," Horne said. "But the lawsuit could have taken another five to six years. By settling now and joining the national settlement, more homeowners will receive help sooner."

Enforcement

The deal establishes a regulatory group of local and federal government agencies. It calls for North Carolina's banking regulator Joseph Smith to monitor lenders for compliance.

Horne said lenders will be subject to hefty fines if they don't follow through with the actions to help homeowners laid out in the settlement.

Federal officials said states could receive more funding if more mortgage firms sign onto the agreement. One estimate is for the national settlement to grow to $40 billion if the next nine large lenders join in. The only state not part of the national settlement is Oklahoma. Arizona, California, Florida, New York and Nevada were the last states to join. Arizona's negotiations with BofA over the mortgage-fraud lawsuit went on until almost 11 p.m. Wednesday night.

President Barack Obama said in a speech Thursday that the $26 billion settlement will allow the nation's biggest banks, "banks rescued by taxpayer dollars," to right wrongs committed in making loans and foreclosing on homeowners during the past several years.

"These banks will put billions of dollars towards relief for families across the nation. They'll provide refinancing for borrowers that are stuck in high interest-rate mortgages," Obama said. "They'll reduce loans for families who owe more on their homes than they're worth. And they will deliver some measure of justice for families that have already been victims of abusive practices."

12 News reporter Melissa Blasius contributed to this article.

by Catherine Reagor - Feb. 9, 2012 09:28 AM The Republic | azcentral.com

Arizona gets $1.6 billion in mortgage fraud settlement

Wednesday, February 8, 2012

PennyMac posts $19.6 million in earnings, plans to expand correspondent lending | HousingWire

PennyMac Mortgage Investment Trust saw its fourth-quarter profit rise as its correspondent lending business surged.

Moorpark, Calif.-based PennyMac posted net income for the fourth-quarter of $19.6 million, or 70 cents a share, beating analysts estimates. That compared to net income of $7.3 million, or 43 cents a share, a year ago.

On average, analysts expected the company to earn 65 cents a share, according to Thomson Reuters I/B/E/S.

For the 2011 fiscal year, PennyMac earned $64.4 million, or $2.41 a share, on total net investment income for the year of $128.6 million.

PennyMac said it expects 2012 mortgage originations in the United States to hit the $1 trillion mark, with $300 million through coorespondent lending. However, new regulatory and capital requirements are causing the big banks to retreat from the mortgage industry, PennyMac said. The result is more opportunity in the mortgage servicing space, the real estate investment trust said, especially with the industry in a period of reform.

"PennyMac will continue to pursue distressed whole loan investments, while also seeking new opportunities, such as mortgage servicing rights," the earnings report states. "Correspondent volume should steadily increase as this becomes a greater component of PennyMac's earnings over the year."

In the most recent fourth quarter, PennyMac's fundings in the correspondent lending side of the business hit $991 million with rate locks of $1.3 billion. Conventional loans made up $566 million of total correspondent funding, followed by Federal Housing Administration loans, which made up $410 million, and jumbo loans, which hit $15 million.

The pre-tax gain of $7.4 million tied to the correspondent lending segment is attributed to conventional and jumbo loans.

During the quarter, PMT agreed to purchase a pool of mortgage loans and REOs with an unpaid principal balance of $49 million. By year end, the company's portfolio of residential mortgage loans, REOs and mortgage-backed securities were valued at $826 million.

Total investment income for 4Q hit $38.7 million.

by Kerri Panchuk Housingwire Feb 8, 2012

PennyMac posts $19.6 million in earnings, plans to expand correspondent lending | HousingWire

Moorpark, Calif.-based PennyMac posted net income for the fourth-quarter of $19.6 million, or 70 cents a share, beating analysts estimates. That compared to net income of $7.3 million, or 43 cents a share, a year ago.

On average, analysts expected the company to earn 65 cents a share, according to Thomson Reuters I/B/E/S.

For the 2011 fiscal year, PennyMac earned $64.4 million, or $2.41 a share, on total net investment income for the year of $128.6 million.

PennyMac said it expects 2012 mortgage originations in the United States to hit the $1 trillion mark, with $300 million through coorespondent lending. However, new regulatory and capital requirements are causing the big banks to retreat from the mortgage industry, PennyMac said. The result is more opportunity in the mortgage servicing space, the real estate investment trust said, especially with the industry in a period of reform.

"PennyMac will continue to pursue distressed whole loan investments, while also seeking new opportunities, such as mortgage servicing rights," the earnings report states. "Correspondent volume should steadily increase as this becomes a greater component of PennyMac's earnings over the year."

In the most recent fourth quarter, PennyMac's fundings in the correspondent lending side of the business hit $991 million with rate locks of $1.3 billion. Conventional loans made up $566 million of total correspondent funding, followed by Federal Housing Administration loans, which made up $410 million, and jumbo loans, which hit $15 million.

The pre-tax gain of $7.4 million tied to the correspondent lending segment is attributed to conventional and jumbo loans.

During the quarter, PMT agreed to purchase a pool of mortgage loans and REOs with an unpaid principal balance of $49 million. By year end, the company's portfolio of residential mortgage loans, REOs and mortgage-backed securities were valued at $826 million.

Total investment income for 4Q hit $38.7 million.

by Kerri Panchuk Housingwire Feb 8, 2012

PennyMac posts $19.6 million in earnings, plans to expand correspondent lending | HousingWire

Tuesday, February 7, 2012

Arizona housing experts guarded but hopeful

No one at this year's Urban Land Institute conference predicted when metro Phoenix's housing market will rebound.

The annual Arizona conference, where real-estate industry leaders convene and predict the market's movements, has been the most important summit on Valley real estate since the beginning of the housing boom nearly a decade ago. But this year, the conversations and atmosphere were different.

The many experts who spoke were more low-key and pragmatic than they'd been during the last five years. Few offered any guesses at when home prices might rebound to boom levels.

That may have been because so many past predictions have been wrong.

At the conference in 2007, the forecast was for metro Phoenix home prices to recover to boom levels by 2010. Instead, prices continued to drop until late last year.

Year after year, as the housing crash and economic downturn worsened, analysts and investors tried to forecast when the market would rebound. By 2011, the mistaken predictions had become a subject of some wry humor.

This year's panel discussions with local and national real-estate investors and developers, held last week in downtown Phoenix, revolved more around hope that the housing market had finally bottomed out. That's because, just as housing helped pull down the rest of the real-estate market, economists and experts believe its recovery will help lead other sectors out of the crash. This idea was echoed again and again during the event.

"Many people believe we are three-fourths through the foreclosures," said Greg Vogel, CEO of Land Advisors, during a discussion on homebuilding. "There's anticipation this spring will be better for housing."

Housing

Metro Phoenix home prices ticked up at the end of last year but are still below 2000's level.

No one at the ULI conference ventured a guess at how long it would take the region's median existing home price to rebound to $267,000, the record it reached in late 2006. The last home-price prediction from the event was last year, when housing analysts called for metro Phoenix home prices to return to pre-boom levels by 2015.

Phoenix's current median existing-home price is $120,000, where it was in 1999. The last pre-boom median is considered to be the 2003 figure -- $155,000.

"Phoenix is in the middle of the pack for a housing recovery," said Steve Hilton, chairman of Scottsdale-based Meritage Homes, comparing the region with other parts of the country.

Homebuilding

For the past few years, the consensus at the ULI conference was that foreclosures would have to slow for home prices to climb and for homebuilding -- a major Valley industry and a source of many jobs -- to begin recovering to pre-boom levels.

Fewer than 7,000 homes were built across the Valley last year, according to the Phoenix Housing Market Letter. That compares with a record 64,000 in 2006. A pre-boom building pace for new homes in the region is closer to 35,000.

Homebuilders at the conference agreed building will pick up this year but said it will be a while before buyers go back out to the fringes of metro Phoenix, no matter how inexpensive the home is or how low gas prices go.

"There are fringe parts of Phoenix where we couldn't make a profit on a new home even if the land was free," said Hilton.

Builders and investors continue to buy land in metro Phoenix in anticipation of the homebuilding market's recovery.

Vogel said $95 million was spent on Phoenix-area home lots ready for construction in 2011.

Apartments

Investors are also buying metro Phoenix apartments again. Developers are building multifamily housing projects, but only in prime central locations. These are positive signs, but none of the apartment experts went as far to say the market was on the rebound.

New complexes, with smaller units and pricier-than-average rents, are going up in central Scottsdale and Phoenix's Biltmore area.

Alliance Residential is building apartments at 25th Street and Camelback Road, where Donald Trump once planned a condominium tower.

Jay Hiemenz of Alliance said when his company committed to the site last year "it was a leap of faith" because Phoenix's apartment market was still struggling.

But Jerry Brand of apartment developer Greystar said Phoenix has great rent-growth potential during the next few years due to the region's increase in renters who either lost homes to foreclosure or don't want to buy no matter how low prices and interest rates fall.

Commercial real estate

Metro Phoenix's retail market started to struggle as soon as residential foreclosures jumped, and it became evident too many speculative homes had been built. Empty shopping centers still dot the Valley in neighborhoods with too many empty homes.

Dan Gardiner, a retail expert with Phoenix Commercial Advisors, said new retail centers went up on the region's fringes right behind the construction of new homes. But when no one moved into the houses, the retailers left or decided not to move in.

He said those neighborhoods will have to fill up before retailers return to those suburbs.

The markets for office and industrial space are more closely tied to Phoenix's job market than its housing market. As the region lost jobs during the recession, offices and warehouses emptied out. The vacancy rate for Valley office space is hovering around 20 percent, according to Phoenix real-estate brokerages.

These two sectors of the real-estate industry are expected to be the last to recover, and the timing depends on metro Phoenix's job growth.

"It's all about putting butts in seats for the office market," said Pete Bolton, managing director of Grubb & Ellis Phoenix. "Phoenix continues to be a cheaper alternative than California for companies transporting and warehousing products."

Christopher Toci of Cushman & Wakefield joked that his market predictions for office and industrial from a few years ago would be correct if you turned them upside down now -- his forecasts for increases were about as big as the market's actual decreases in leasing and sales.

The final takeaway from the conference was that growth would continue in metro Phoenix, but it would be slower than expected and different from past cycles.

"The balance between new housing near new jobs is more important than ever," said Steve Betts, chairman of ULI Arizona.

Unlike last year or 2009, the experts gave up on predicting the timing of a recovery and focused on the first real positive market signs they have seen in years.

"The new homes we sold in 2005, we re-bought in 2007," said Drew Brown, chairman of Scottsdale-based DMB Associates, developer of Verrado in Buckeye and DC Ranch in Scottsdale. "Now, we are finally selling those homes again."

by Catherine Reagor - Feb. 3, 2012 11:21 PM The Republic | azcentral.com

Arizona housing experts guarded but hopeful

The annual Arizona conference, where real-estate industry leaders convene and predict the market's movements, has been the most important summit on Valley real estate since the beginning of the housing boom nearly a decade ago. But this year, the conversations and atmosphere were different.

The many experts who spoke were more low-key and pragmatic than they'd been during the last five years. Few offered any guesses at when home prices might rebound to boom levels.

That may have been because so many past predictions have been wrong.

At the conference in 2007, the forecast was for metro Phoenix home prices to recover to boom levels by 2010. Instead, prices continued to drop until late last year.

Year after year, as the housing crash and economic downturn worsened, analysts and investors tried to forecast when the market would rebound. By 2011, the mistaken predictions had become a subject of some wry humor.

This year's panel discussions with local and national real-estate investors and developers, held last week in downtown Phoenix, revolved more around hope that the housing market had finally bottomed out. That's because, just as housing helped pull down the rest of the real-estate market, economists and experts believe its recovery will help lead other sectors out of the crash. This idea was echoed again and again during the event.

"Many people believe we are three-fourths through the foreclosures," said Greg Vogel, CEO of Land Advisors, during a discussion on homebuilding. "There's anticipation this spring will be better for housing."

Housing

Metro Phoenix home prices ticked up at the end of last year but are still below 2000's level.

No one at the ULI conference ventured a guess at how long it would take the region's median existing home price to rebound to $267,000, the record it reached in late 2006. The last home-price prediction from the event was last year, when housing analysts called for metro Phoenix home prices to return to pre-boom levels by 2015.

Phoenix's current median existing-home price is $120,000, where it was in 1999. The last pre-boom median is considered to be the 2003 figure -- $155,000.

"Phoenix is in the middle of the pack for a housing recovery," said Steve Hilton, chairman of Scottsdale-based Meritage Homes, comparing the region with other parts of the country.

Homebuilding

For the past few years, the consensus at the ULI conference was that foreclosures would have to slow for home prices to climb and for homebuilding -- a major Valley industry and a source of many jobs -- to begin recovering to pre-boom levels.

Fewer than 7,000 homes were built across the Valley last year, according to the Phoenix Housing Market Letter. That compares with a record 64,000 in 2006. A pre-boom building pace for new homes in the region is closer to 35,000.

Homebuilders at the conference agreed building will pick up this year but said it will be a while before buyers go back out to the fringes of metro Phoenix, no matter how inexpensive the home is or how low gas prices go.

"There are fringe parts of Phoenix where we couldn't make a profit on a new home even if the land was free," said Hilton.

Builders and investors continue to buy land in metro Phoenix in anticipation of the homebuilding market's recovery.

Vogel said $95 million was spent on Phoenix-area home lots ready for construction in 2011.

Apartments

Investors are also buying metro Phoenix apartments again. Developers are building multifamily housing projects, but only in prime central locations. These are positive signs, but none of the apartment experts went as far to say the market was on the rebound.

New complexes, with smaller units and pricier-than-average rents, are going up in central Scottsdale and Phoenix's Biltmore area.

Alliance Residential is building apartments at 25th Street and Camelback Road, where Donald Trump once planned a condominium tower.

Jay Hiemenz of Alliance said when his company committed to the site last year "it was a leap of faith" because Phoenix's apartment market was still struggling.

But Jerry Brand of apartment developer Greystar said Phoenix has great rent-growth potential during the next few years due to the region's increase in renters who either lost homes to foreclosure or don't want to buy no matter how low prices and interest rates fall.

Commercial real estate

Metro Phoenix's retail market started to struggle as soon as residential foreclosures jumped, and it became evident too many speculative homes had been built. Empty shopping centers still dot the Valley in neighborhoods with too many empty homes.

Dan Gardiner, a retail expert with Phoenix Commercial Advisors, said new retail centers went up on the region's fringes right behind the construction of new homes. But when no one moved into the houses, the retailers left or decided not to move in.

He said those neighborhoods will have to fill up before retailers return to those suburbs.

The markets for office and industrial space are more closely tied to Phoenix's job market than its housing market. As the region lost jobs during the recession, offices and warehouses emptied out. The vacancy rate for Valley office space is hovering around 20 percent, according to Phoenix real-estate brokerages.

These two sectors of the real-estate industry are expected to be the last to recover, and the timing depends on metro Phoenix's job growth.

"It's all about putting butts in seats for the office market," said Pete Bolton, managing director of Grubb & Ellis Phoenix. "Phoenix continues to be a cheaper alternative than California for companies transporting and warehousing products."

Christopher Toci of Cushman & Wakefield joked that his market predictions for office and industrial from a few years ago would be correct if you turned them upside down now -- his forecasts for increases were about as big as the market's actual decreases in leasing and sales.

The final takeaway from the conference was that growth would continue in metro Phoenix, but it would be slower than expected and different from past cycles.

"The balance between new housing near new jobs is more important than ever," said Steve Betts, chairman of ULI Arizona.

Unlike last year or 2009, the experts gave up on predicting the timing of a recovery and focused on the first real positive market signs they have seen in years.

"The new homes we sold in 2005, we re-bought in 2007," said Drew Brown, chairman of Scottsdale-based DMB Associates, developer of Verrado in Buckeye and DC Ranch in Scottsdale. "Now, we are finally selling those homes again."

by Catherine Reagor - Feb. 3, 2012 11:21 PM The Republic | azcentral.com

Arizona housing experts guarded but hopeful

Apartments are planned

A four-story, 274-unit apartment complex would replace Plaza 777 on the southern edge of downtown Scottsdale under plans recently submitted.

The proposed Bauhaus Flats & Studios would be built on 4.4 acres northeast of Scottsdale and Thomas roads and on an adjacent ¾-acre parcel on 73rd Street. It would include about 10,000 square feet of commercial space.

The shopping plaza, built in 1960, includes a florist, locksmith, rental-car agency, restaurant, hobby shop and Plato's Closet clothing store. More than half of the 40,251-square-foot plaza is vacant.

Architect Kristjan Sigurdsson of K&I Homes LLC said there is high demand for apartments in the area because virtually no units have been built downtown in the last decade.

"This would be a nice addition to that whole housing market," he said, adding that the Bauhaus apartments would be within walking distance of neighborhood commercial services.

The area has a diverse mix that includes a supermarket, hardware store, coffee shop, bowling alley, adult bookstore, car wash, bail bondsman and pawnshops.

The Sphinx Ranch Gourmet Gift Market, which has operated in the Valley for 61 years, is two doors to the north. Jason Heetland, Sphinx Ranch owner, said it's time for something to be done to update the area.

"I would hope that the current tenants would have a first right of refusal to lease space" in the Bauhaus' shops, Heetland said.

Area business owners have struggled for nearly a year with Scottsdale Road streetscape improvements, he said. The developers are seeking a rezoning for the Plaza 777 site from commercial to planned-unit development.

The development team includes architect Sigurdsson, Tom Frankel and Keith Nygren. KT777 LLC bought the plaza for $2.58 million.

No date has been set for the rezoning hearings.

by Peter Corbett - Feb. 3, 2012 02:33 PM The Republic | azcentral.com

Apartments are planned

The proposed Bauhaus Flats & Studios would be built on 4.4 acres northeast of Scottsdale and Thomas roads and on an adjacent ¾-acre parcel on 73rd Street. It would include about 10,000 square feet of commercial space.

The shopping plaza, built in 1960, includes a florist, locksmith, rental-car agency, restaurant, hobby shop and Plato's Closet clothing store. More than half of the 40,251-square-foot plaza is vacant.

Architect Kristjan Sigurdsson of K&I Homes LLC said there is high demand for apartments in the area because virtually no units have been built downtown in the last decade.

"This would be a nice addition to that whole housing market," he said, adding that the Bauhaus apartments would be within walking distance of neighborhood commercial services.

The area has a diverse mix that includes a supermarket, hardware store, coffee shop, bowling alley, adult bookstore, car wash, bail bondsman and pawnshops.

The Sphinx Ranch Gourmet Gift Market, which has operated in the Valley for 61 years, is two doors to the north. Jason Heetland, Sphinx Ranch owner, said it's time for something to be done to update the area.

"I would hope that the current tenants would have a first right of refusal to lease space" in the Bauhaus' shops, Heetland said.

Area business owners have struggled for nearly a year with Scottsdale Road streetscape improvements, he said. The developers are seeking a rezoning for the Plaza 777 site from commercial to planned-unit development.

The development team includes architect Sigurdsson, Tom Frankel and Keith Nygren. KT777 LLC bought the plaza for $2.58 million.

No date has been set for the rezoning hearings.

by Peter Corbett - Feb. 3, 2012 02:33 PM The Republic | azcentral.com

Apartments are planned

Foreclosures hit 4-year low in metro area

New data indicate that the number of Phoenix-area homes taken back by lenders in January fell to its lowest level since early 2008.

Last month, there were 2,263 foreclosures, or trustee sales, in the region, according to real-estate research firm Information Market. Pre-foreclosures, also known as notice of trustee sales, fell to 2,932, the lowest level since the summer of 2007.

A year ago, both foreclosures and pre-foreclosures were double what they are now. The number of pending foreclosures is one-third of what it was a year ago. Only 15,000 active foreclosures are making their way through the process now.

Some housing analysts continue to talk about shadow inventory, characterized as essentially unexpected foreclosures that will hit the market just as it begins to recover. But that phenomenon can't be tracked now.

Tom Ruff, analyst with Information Market, tracks notice of trustee sales, trustee sales and homes sold at the foreclosure auction daily. He said he sees no sign of a shadow-inventory problem in metro Phoenix.

The region's mortgage-delinquency rate has also fallen during the past year, meaning fewer homeowners are falling behind on their payments. Some market watchers say banks just aren't moving on many foreclosures and are not reporting all the loans borrowers are missing payments on, but lenders deny this.